Full Report

The numbers behind Adobe Inc.: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in US$ millions unless noted.

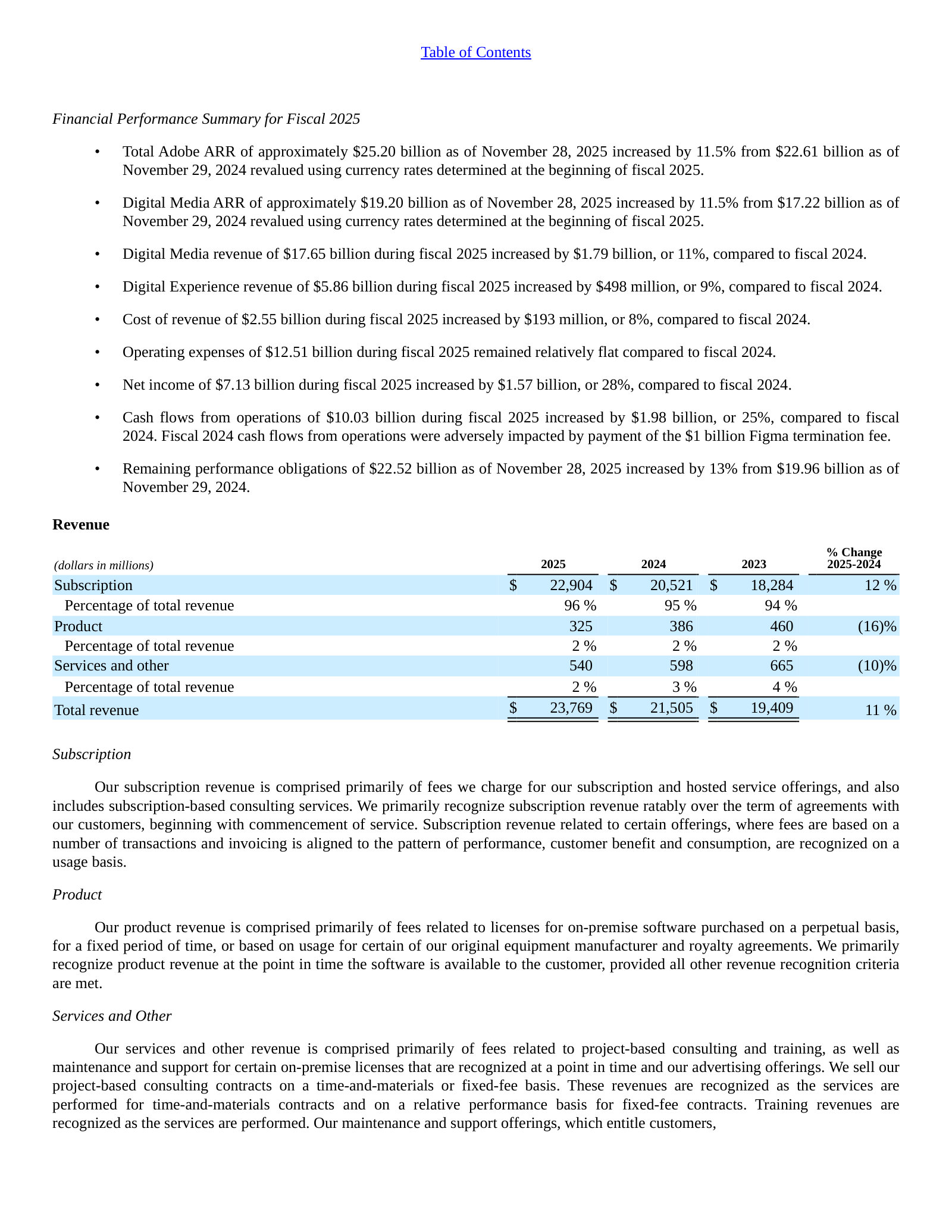

Reading notes: Reporting currency US dollars; all figures in millions except per-share data, as printed in Adobe's Forms 10-K. Adobe's fiscal year ends on the Friday nearest November 30 (fiscal 2025 ended November 28, 2025). FY2025, FY2024 and FY2023 columns are the three years printed in the FY2025 Form 10-K (income statement and cash flows). FY2023 balance-sheet figures are the comparative column of the FY2024 Form 10-K (the FY2025 10-K balance sheet shows only FY2025 and FY2024). FY2022 and FY2021 columns are the two most recent years printed in the FY2022 Form 10-K (FY2021 is that filing's comparative column; Adobe also filed a standalone FY2021 10-K with identical audited figures). Segment revenue and gross profit use Adobe's three reportable segments — Digital Media, Digital Experience, and Publishing and Advertising — as disclosed in the segment note. The income statement itself disaggregates revenue only by Subscription / Product / Services and other.

Share Price — Full Available History — 37 Years

The stock closed at $237.25 on Jul 17, 2026 — up 299,830% over the window shown (+24.5% a year), trading between $0.07 and $688.37. At that close the stock trades at 14× FY2025 diluted EPS as reported below.

Source: market price feed, monthly closes, sampled from 9,202 source observations, Jan 1990–Jul 2026. Price return only, excludes dividends. Prices are split-adjusted (1:2 on Aug 11, 1993; 1:2 on Oct 27, 1999; 1:2 on Oct 25, 2000; 1:2 on May 24, 2005).

FY2025 at a Glance

Revenue (US$ millions)

Operating income (US$ millions)

Net income (US$ millions)

Diluted EPS

Source: FY2025 consolidated statements [1] [2]. Click any linked figure to open the filing page with the row highlighted.

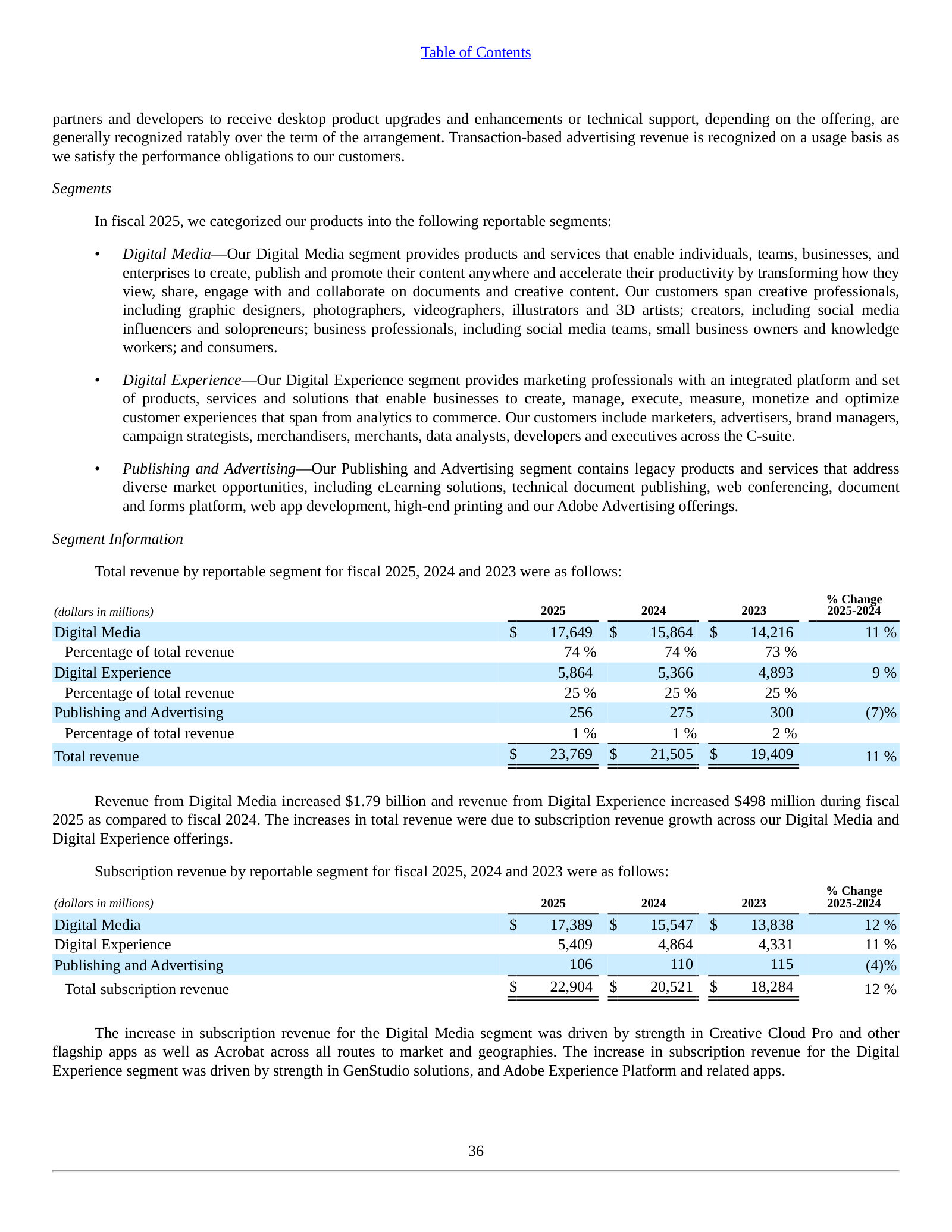

Revenue by Segment

| Revenue by Segment | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Digital Media | 11,520 | 12,842 | 14,216 | 15,864 | 17,649 |

| Digital Experience | 3,867 | 4,422 | 4,893 | 5,366 | 5,864 |

| Publishing and Advertising | 398 | 342 | 300 | 275 | 256 |

| Total revenue | 15,785 | 17,606 | 19,409 | 21,505 | 23,769 |

| Total revenue growth, derived | — | +11.5% | +10.2% | +10.8% | +10.5% |

Source: Note 14 Segment and Geographic Information; Consolidated Statements of Income [3] [1] [4] [2]. Click any linked figure to open the filing page with the row highlighted.

Gross Profit by Segment

| Gross Profit by Segment | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Digital Media | 11,091 | 12,281 | 13,551 | 15,184 | 16,808 |

| Digital Experience | 2,546 | 2,920 | 3,290 | 3,777 | 4,239 |

| Publishing and Advertising | 283 | 240 | 214 | 186 | 171 |

| Total gross profit | 13,920 | 15,441 | 17,055 | 19,147 | 21,218 |

Source: Note 14 Segment and Geographic Information [3] [1] [4] [2]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Income [1] [2]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-18. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets [5] [6] [7]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows [8] [9]. Click any linked figure to open the filing page with the row highlighted.

Digital Media ARR Engine

| Digital Media ARR Engine | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Digital Media ARR (ending) | 12,240 | 13,970 | 15,170 | 17,330 | 19,200 |

| Digital Media ARR growth (YoY) | 19.0% | 15.0% | 14.0% | 13.0% | 11.5% |

| Creative ARR | 10,300 | 11,600 | 12,370 | 13,850 | — |

| Document Cloud ARR | 1,930 | 2,370 | 2,810 | 3,480 | — |

| Total Adobe ending ARR | — | — | — | — | 25,200 |

Source: company filings [10] [11] [12] [13]. Click any linked figure to open the filing page with the row highlighted.

Recurring Revenue Backlog

| Recurring Revenue Backlog | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Subscription revenue | 14,573 | 16,388 | 18,284 | 20,521 | 22,904 |

| Subscription revenue (% of total) | 92.0% | 93.0% | 94.0% | 95.0% | 96.0% |

| Remaining performance obligations | 13,990 | 15,190 | 17,220 | 19,960 | 22,520 |

Source: company filings [14] [15] [16]. Click any linked figure to open the filing page with the row highlighted.

Revenue by Geography

| Revenue by Geography | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Americas | 8,996 | 10,251 | 11,654 | 12,891 | 14,120 |

| EMEA | 4,252 | 4,593 | 4,881 | 5,554 | 6,289 |

| APAC | 2,537 | 2,762 | 2,874 | 3,060 | 3,360 |

Source: company filings [17] [18]. Click any linked figure to open the filing page with the row highlighted.

Workforce Capital Return

| Workforce Capital Return | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Employees (headcount) | 25,988 | 29,239 | 29,945 | 30,709 | 31,360 |

| Stock-based compensation | 1,090 | 1,440 | 1,718 | 1,833 | 1,942 |

| Remaining stock repurchase authorization | — | — | — | — | 5,900 |

Source: company filings [19] [20] [21] [22]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Operating income | Net income | Diluted earnings per share | Operating cash flow |

|---|---|---|---|---|---|

| FY2016 | 5,854 | 1,494 | 1,169 | 2.32 | 2,200 |

| FY2017 | 7,302 | 2,168 | 1,694 | 3.38 | 2,913 |

| FY2018 | 9,030 | 2,840 | 2,591 | 5.20 | 4,029 |

| FY2019 | 11,171 | 3,268 | 2,951 | 6.00 | 4,422 |

| FY2020 | 12,868 | 4,237 | 5,260 | 10.83 | 5,727 |

| FY2021 | 15,785 | 5,802 | 4,822 | 10.02 | 7,230 |

| FY2022 | 17,606 | 6,098 | 4,756 | 10.10 | 7,838 |

| FY2023 | 19,409 | 6,650 | 5,428 | 11.82 | 7,302 |

| FY2024 | 21,505 | 6,741 | 5,560 | 12.36 | 8,056 |

| FY2025 | 23,769 | 8,706 | 7,130 | 16.70 | 10,031 |

Source: consolidated statements across filings; older years from the standardized feed [8] [1] [9] [2]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-18. Estimate figures link to the consensus source, not to filing pages.

Traceability

349 of 378 figures on this page (92%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

Reporting currency US dollars; all figures in millions except per-share data, as printed in Adobe's Forms 10-K. Adobe's fiscal year ends on the Friday nearest November 30 (fiscal 2025 ended November 28, 2025).

FY2025, FY2024 and FY2023 columns are the three years printed in the FY2025 Form 10-K (income statement and cash flows). FY2023 balance-sheet figures are the comparative column of the FY2024 Form 10-K (the FY2025 10-K balance sheet shows only FY2025 and FY2024).

FY2022 and FY2021 columns are the two most recent years printed in the FY2022 Form 10-K (FY2021 is that filing's comparative column; Adobe also filed a standalone FY2021 10-K with identical audited figures).

Segment revenue and gross profit use Adobe's three reportable segments — Digital Media, Digital Experience, and Publishing and Advertising — as disclosed in the segment note. The income statement itself disaggregates revenue only by Subscription / Product / Services and other.

FY2016–FY2020 long-term-record figures are from the standardized SEC XBRL data feed and are shown without page links.

Remaining performance obligations (RPO) were approximately $22.52 billion as of November 28, 2025 (FY2025 10-K, Note on Deferred Revenue and Remaining Performance Obligations); disclosed as a single-year prose figure, so not tabulated as a multi-year KPI.

The FY2024 'Acquisition termination fee' of $1,000 million is the one-time fee Adobe paid on the terminated Figma acquisition; it appears as a discrete operating-expense line only in the FY2024/FY2025 10-K income statements.

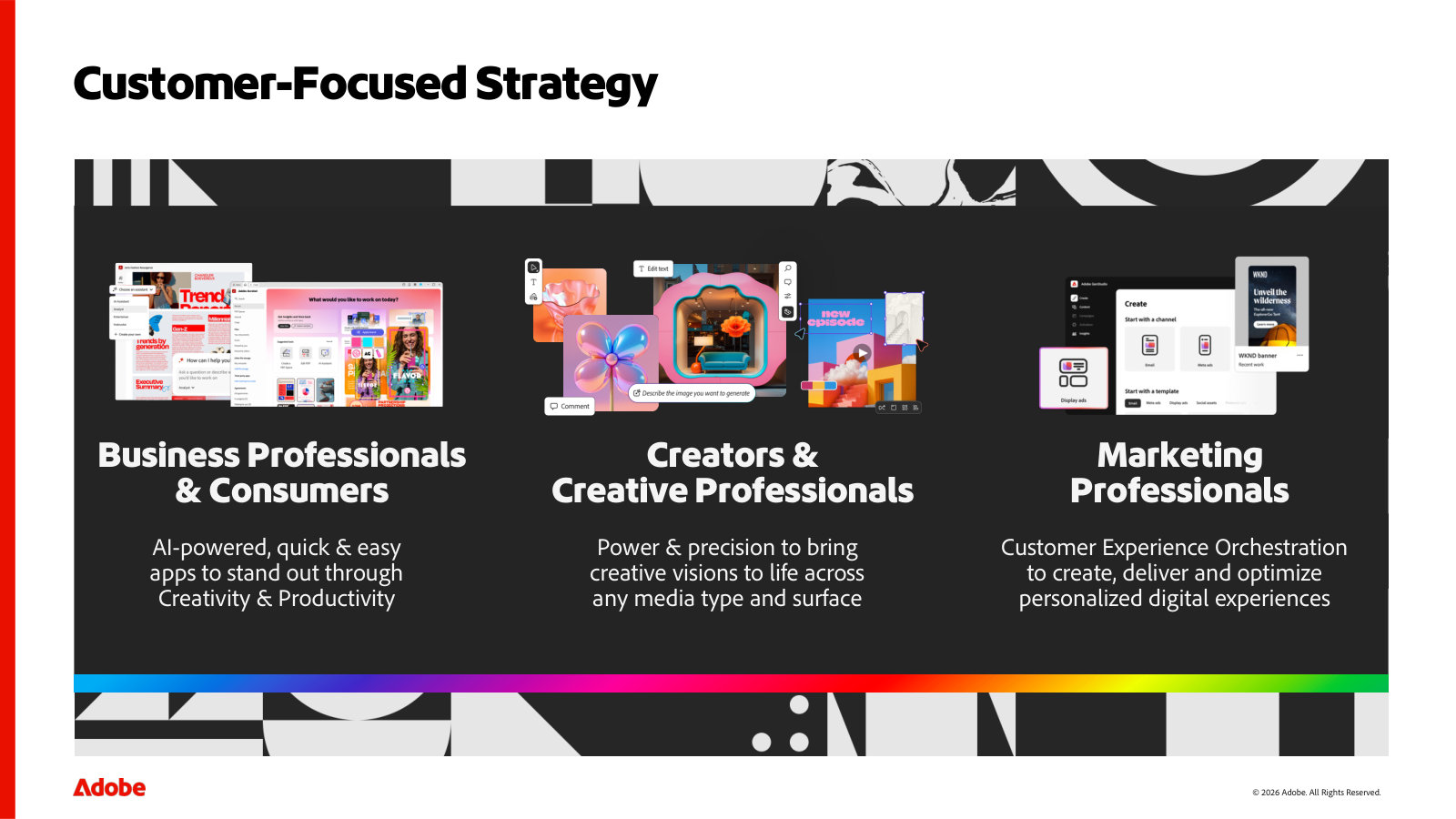

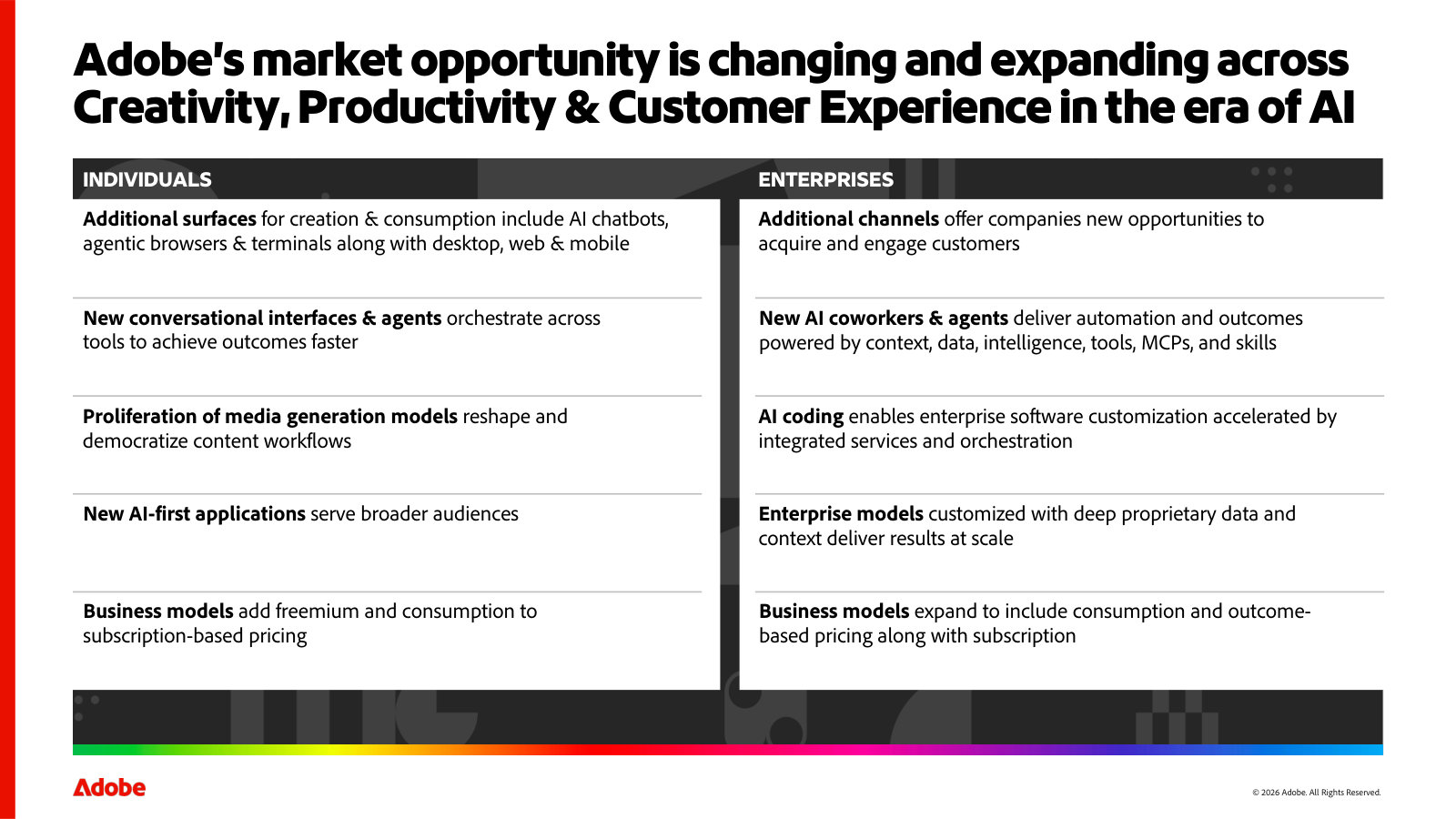

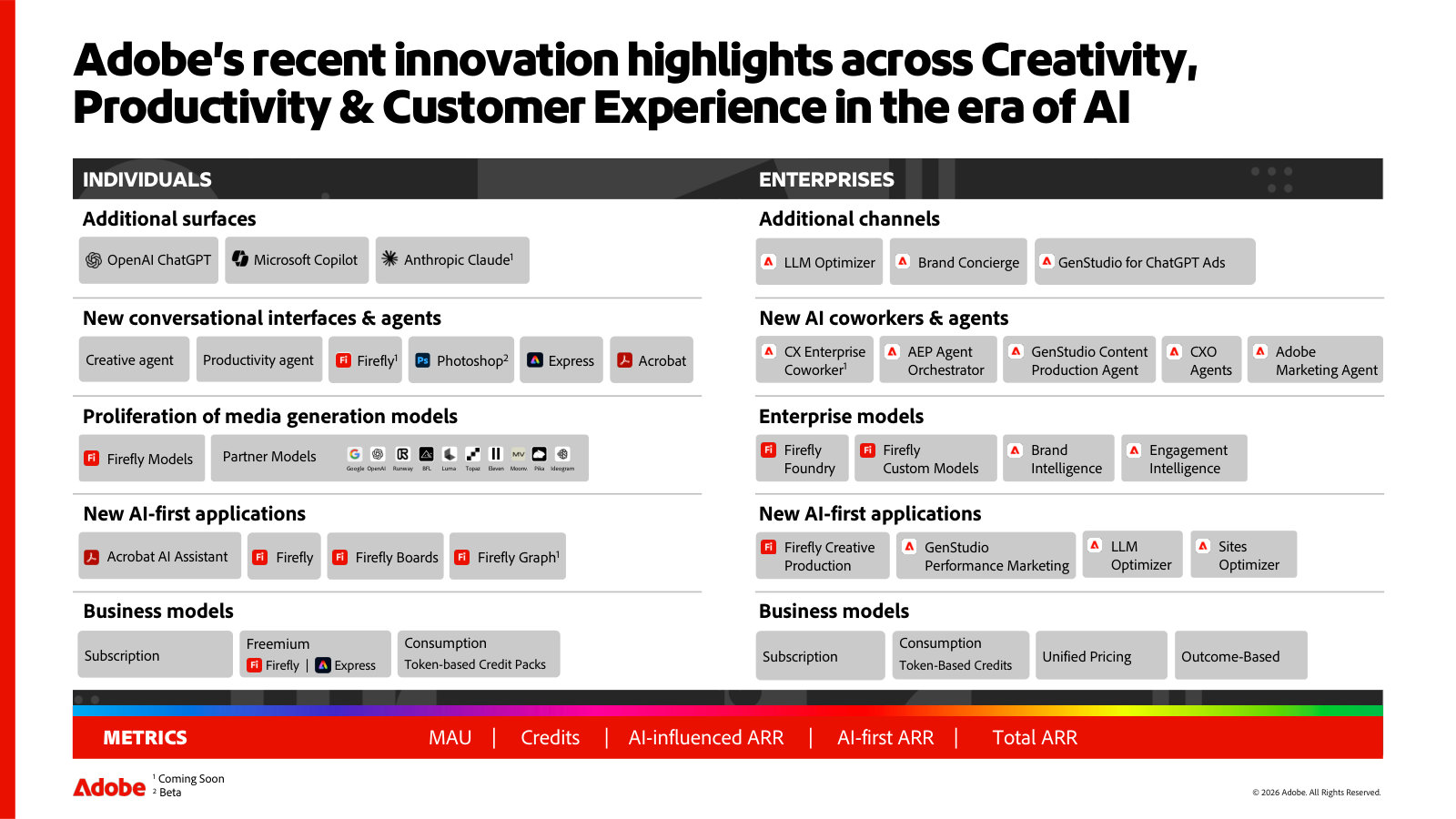

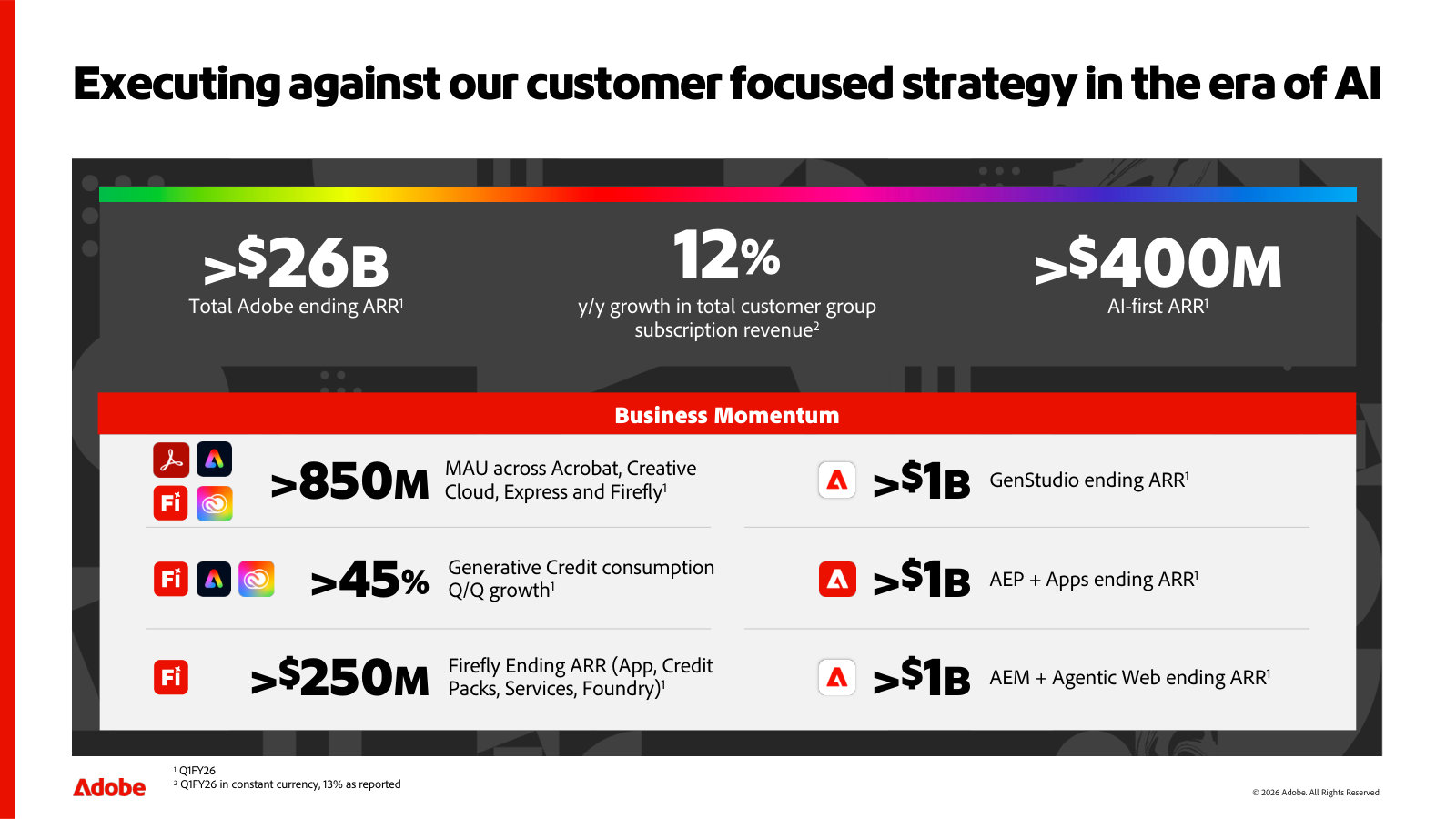

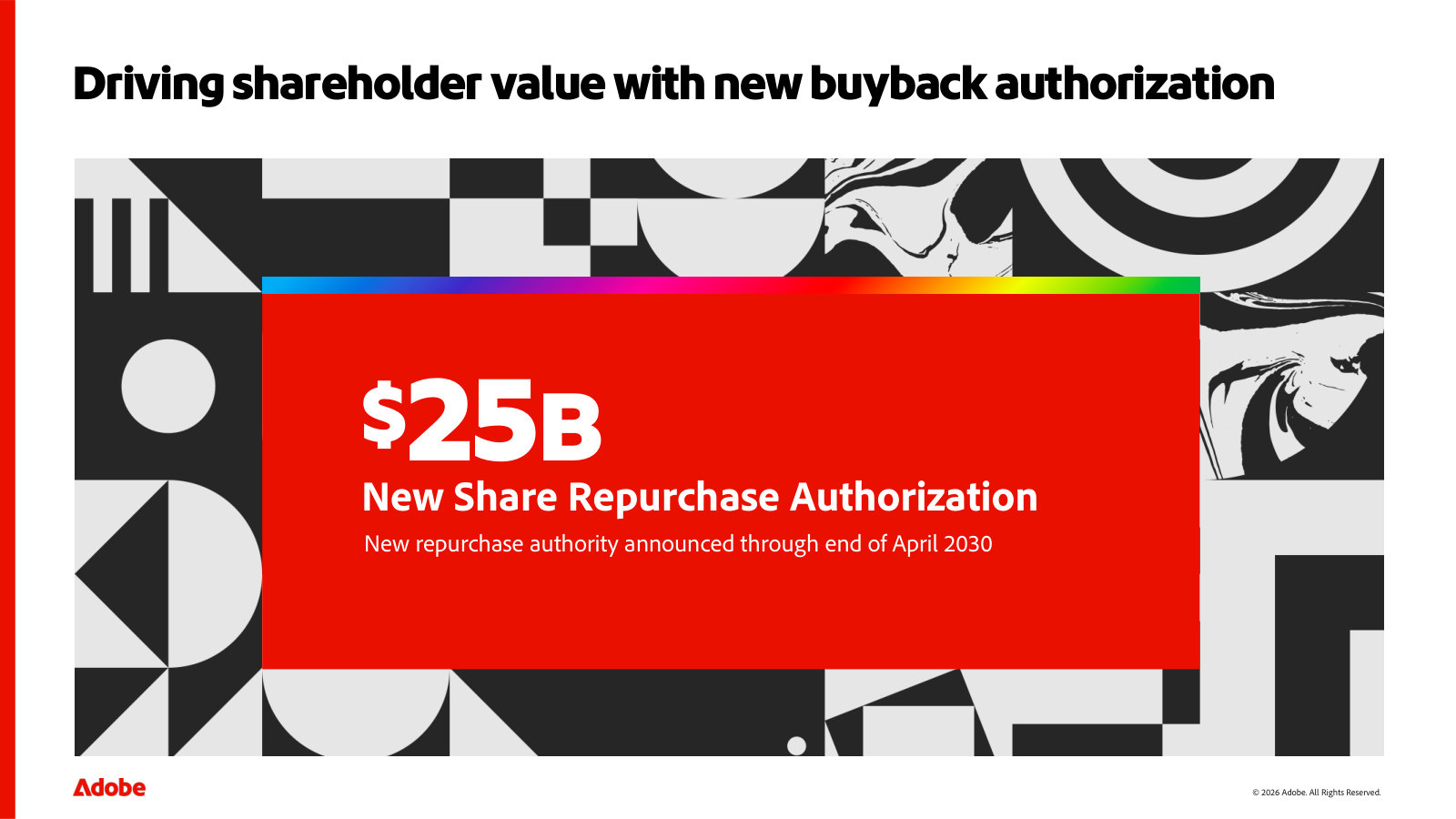

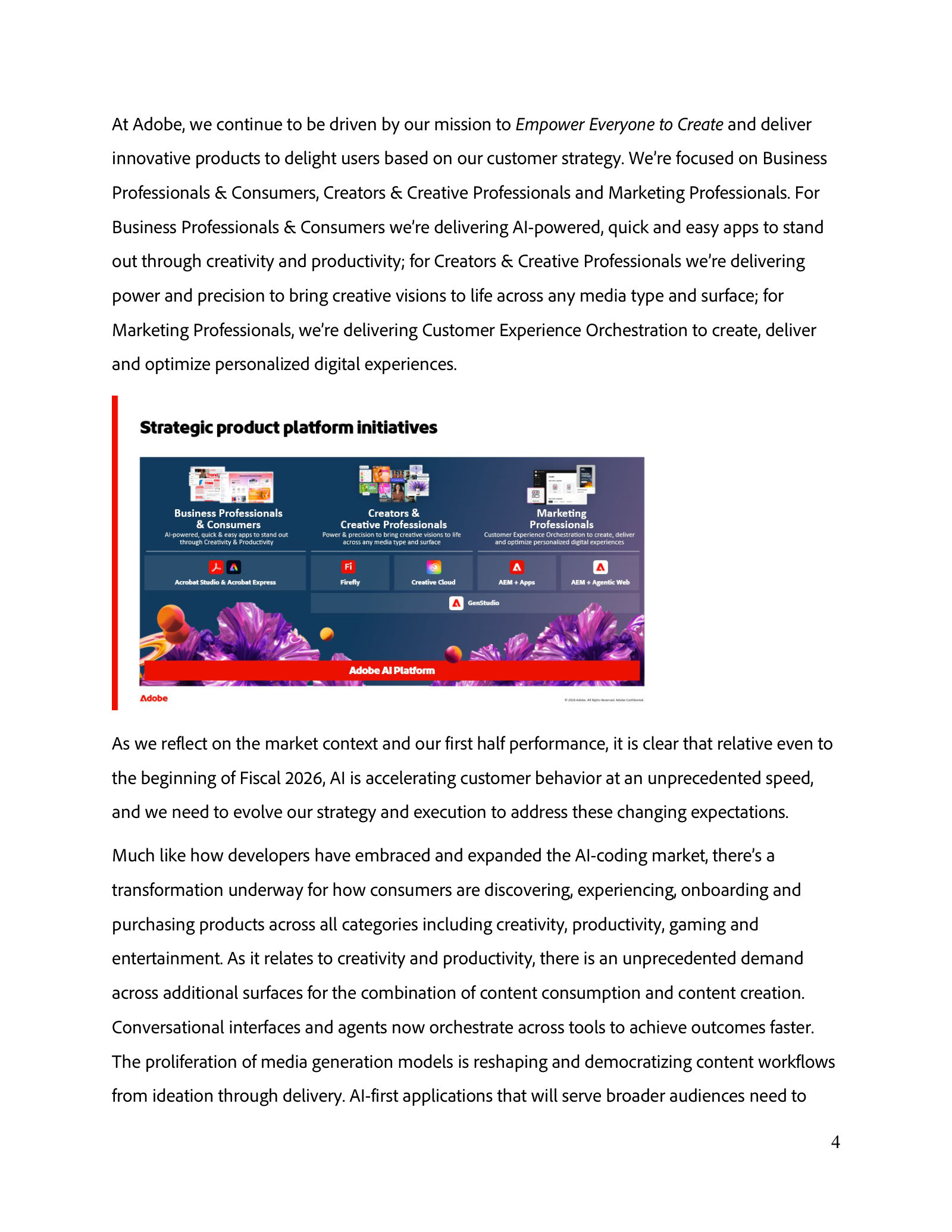

Adobe Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

Investor Summit Q&A — 2026

Management's fullest current overview — mission, the AI-era market opportunity, the product portfolio, business momentum and capital return. · Open the full document →

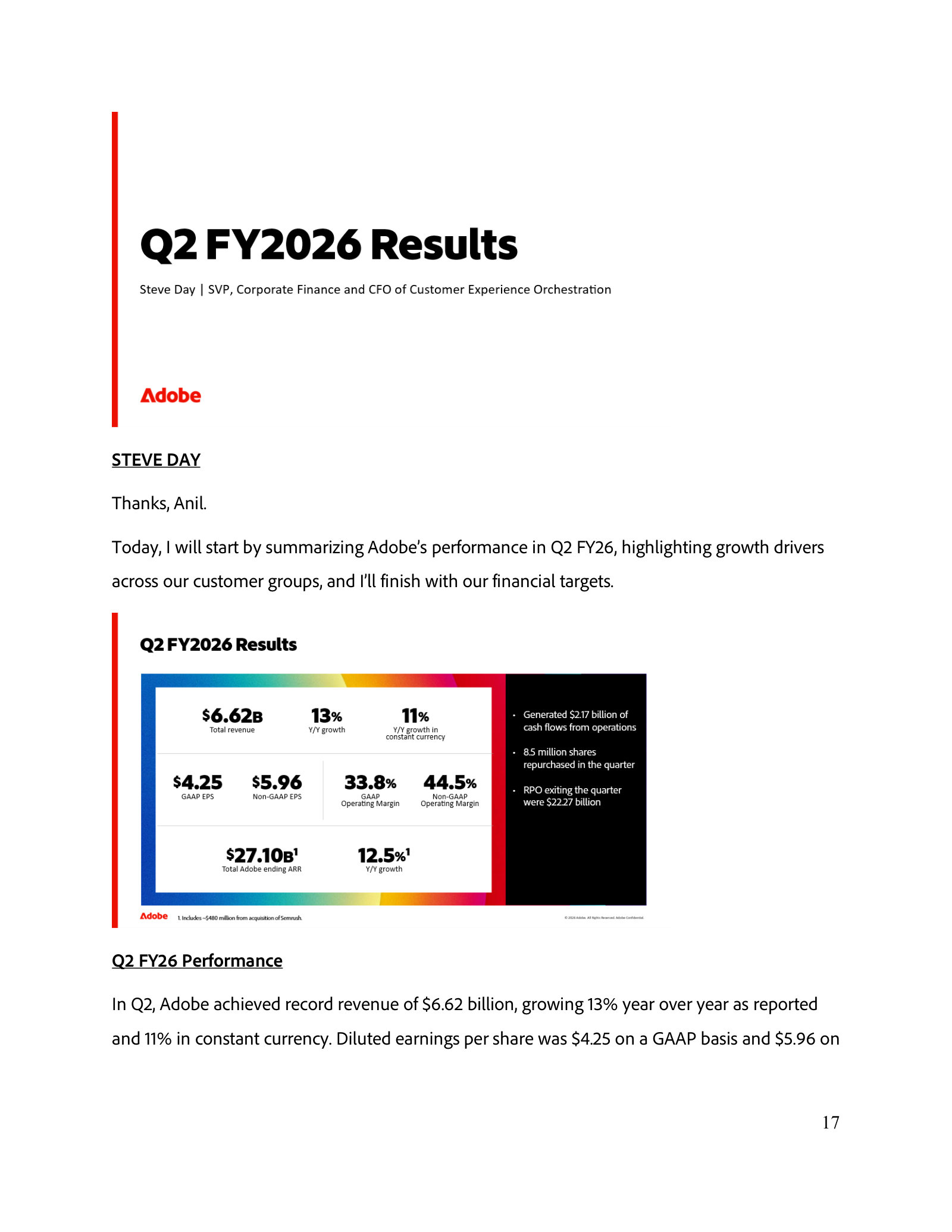

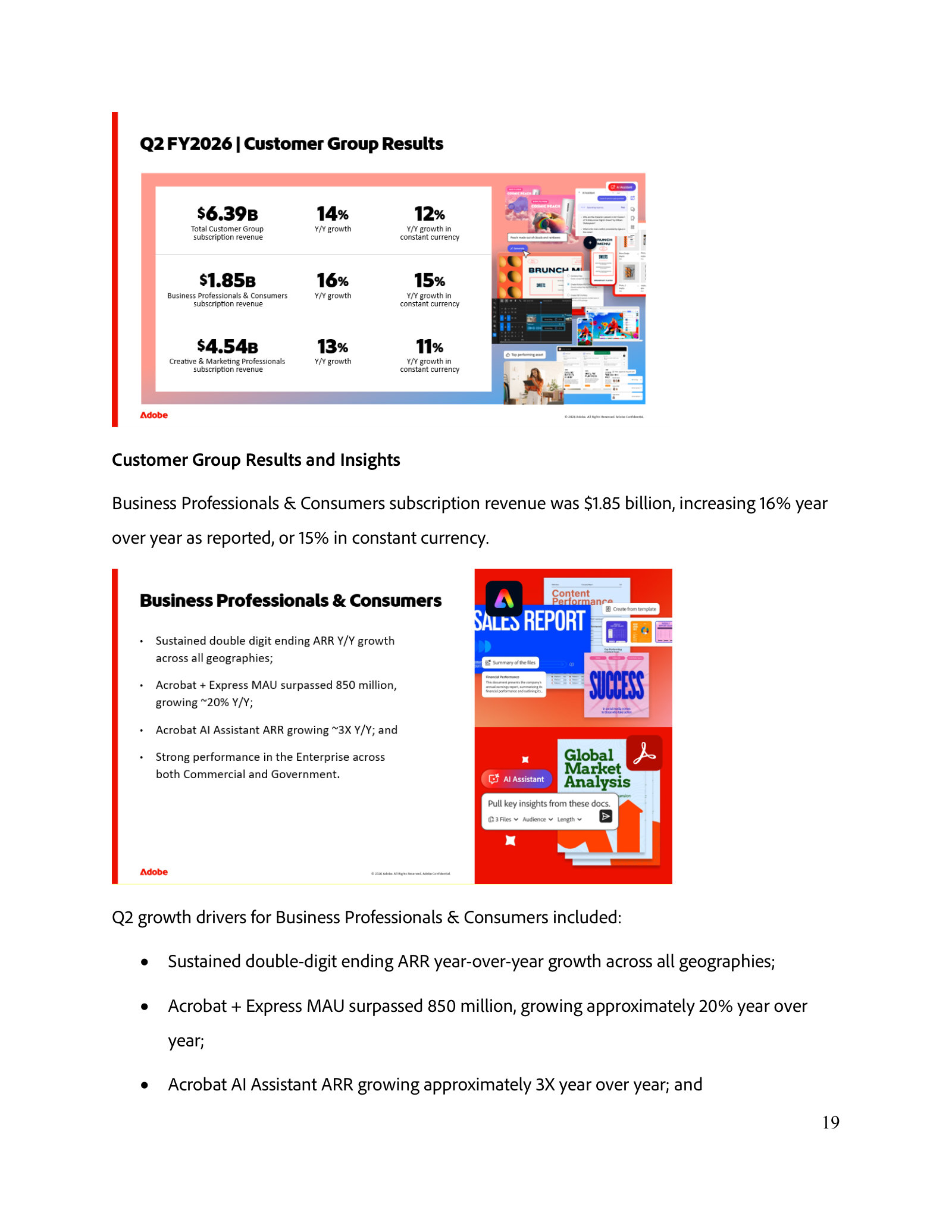

Q2 FY2026 Earnings Call — Q2 FY2026

The latest quarterly deck: current financials, the product-to-segment map, and revenue split across the two reported customer groups. · Open the full document →

More from management

Q4 & Full-Year FY2025 Earnings Call — Q4 FY2025 · 29 pages · Full-year FY2025 results, the announced Semrush acquisition, and the initial FY2026 revenue, ARR and EPS targets management set. · Open →

Q4 & Full-Year FY2024 Earnings Call — Q4 FY2024 · 24 pages · The FY2024 full-year results and the FY2025 targets that framed the prior year's plan — a baseline for measuring progress. · Open →

Adobe Inc.'s management answers for the business every quarter. These are the exchanges that explain it best — verbatim, from the call transcripts preserved in Sources. Each link opens the full transcript at that page in a new tab.

Q2 FY2026 Earnings Call — June 11, 2026

The strategic reset: management chooses to route surging AI traffic into a free Firefly/Express funnel — knowingly cutting second-half ARR — while a CFO exit and a CEO succession are underway, and fields the sharpest 'why now, and what's the payback' pushback. · Open the full transcript →

The pivot thesis: AI is changing buyer behavior so fast that the near-term prize is free user acquisition, not immediate paid conversion.

Shantanu Narayen, Chair & CEO: As we reflect on the market context and our first half performance, it is clear that relative even to the beginning of fiscal 26, AI is accelerating customer behavior at an unprecedented speed and we need to evolve our strategy and execution to address these changing expectations. […] Big picture, the immediate opportunity for Adobe is to accelerate new user acquisition and lifetime value through a freemium offering.

p. 1 · Read in context →

The one number that anchors the bull case: AI-first ARR tripled year-over-year to over $500 million.

Shantanu Narayen, Chair & CEO: Adobe's AI innovation has driven an impressive 3x year-over-year increase in AI-first ARR to greater than $500 million. We believe now is the time to aggressively acquire the next generation of Adobe loyalists.

p. 2 · Read in context →

The candid cost and the leadership overhang: the freemium shift lowers 2H ARR, the CFO is departing, and a CEO search is live.

Shantanu Narayen, Chair & CEO: The strategic shift to acquire more freemium customers through Adobe and Firefly lowers our second half ARR growth expectations from individual subscribers. […] As we announced, Daniel Durn has decided to pursue a new opportunity outside the software industry. I would like to thank Daniel for his contributions to Adobe and wish him well. […] Given my decision to transition to Board Chair, I wanted to provide an update on the CEO search, which is progressing well.

p. 3 · Read in context →

How the funnel actually works: rank for an intent search ('summarize this PDF'), do the task free, build a habit, then paywall.

David Wadhwani, President of Creativity & Productivity: We see a shift to LLM usage driving intent-based search. Someone might type into a search engine, 'summarize this PDF.' We use SEO and SEM capabilities to rank high for that query. When the user clicks our link, we take them directly into Acrobat web with a single call to action: upload your PDF, and we summarize it for them. When we summarize it, we introduce them to the AI Assistant so they can ask questions. We use this process to let them build a habit before we start applying a paywall.

p. 8 · Read in context →

Q4 & FY2025 Earnings Call — December 10, 2025

The full-year proof-point call: FY25 revenue of $23.77B with AI-influenced ARR now over a third of the book, a record FY26 net-new-ARR guide, and the clearest walk-throughs of how Firefly Foundry and generative credits actually monetize. · Open the full transcript →

The FY25 scoreboard, framed around AI: record $23.77B revenue and $20.94 non-GAAP EPS, with AI-first ARR accelerating through the year.

Shantanu Narayen, CEO: In fiscal 2025, Adobe delivered significant AI-influenced and AI-first ending ARR, which accelerated through the year. We achieved record revenue of $23.77 billion and non-GAAP EPS of $20.94, which represents outstanding financial performance.

p. 1 · Read in context →

Firefly Foundry economics: a media customer spending ~$10M on core creative added ~$7M for custom-model services after a six-month sale.

David Wadhwani, President of Digital Media: let's say that that organization was spending $10 million with us ARR on our core creative products that we've been selling with them. We ran a sales process with them and gave engagement with them for about six months. We were able to sell them Firefly services Firefly Foundry for about $7 million, so pretty significant step up in terms of, you know, the engagement that we have with the customer.

p. 7 · Read in context →

The recurring bear case: when does all this AI usage finally show up as stable or accelerating ARR? Narayen argues Q4 is that inflection.

Keith Weiss (Morgan Stanley); Shantanu Narayen, CEO: When can we potentially see this sort of grow the totality or stabilize or accelerate the totality of growth? At Adobe. Meaning, another when we see a year where ARR growth is stable, right, on a year-on year basis or actually improving, because I think that's what investors really wanna see to get more confident in the stock and start revisiting the stock and coming back to the shares? […] Q4 was a really strong quarter. And frankly, starting to be this inflection in terms of as we see the leading indicators. What is happening across the leading indicators. You know, which gives us a lot of confidence.

p. 9 · Read in context →

How generative AI monetizes: base credits per plan, then upgrades or add-on packs; a multiplier of apps, media, use cases and models.

David Wadhwani, President of Digital Media: we introduced, generative credits a few years ago when we introduced, generative AI into our products. And customers get credits in a couple of different ways. First, you know, all of our plans now come with some base level of credit, access. And, of course, higher-end plans include more credits. The second thing is that when customers deplete their credits, they can get more credits in one of two ways. They can upgrade to a higher-end plan, and or they can purchase generative credit add-on pack. And as we think about the growth algorithm associated with this, it's really a multiplier across four different things. First of all, the number of apps that have these generative capabilities, times the number of media types that we support, times the number of use cases and workflows that we've integrated these into, times the number of models that we have that people are able to use.

p. 11 · Read in context →

Q4 & FY2024 Earnings Call — December 11, 2024

A record year that the market hated: after $2B in net-new Digital Media ARR, the FY25 guide implied deceleration and the stock sank. Home to the bluntest 'is there a leak in the bucket?' challenge and Adobe's clearest growth-algorithm answer. · Open the full transcript →

The paradox in one line: a record FY24 — $21.5B revenue and the first-ever $2B of net-new Digital Media ARR — set against a falling stock.

Shantanu Narayen, CEO: 2024 was a year of records for Adobe. We achieved record revenue of $21.51 billion, representing 11% year-over-year growth. […] We had several new milestones with our AI innovations enabling us to add more than $2 billion in digital media net new ARR and surpass $1 billion in the ending book of business for Adobe Experience Platform and native apps.

p. 1 · Read in context →

The Digital Media growth algorithm, 'p times q plus v' — new users, price/value, enterprise value — and why FY25 tilts to new users.

David Wadhwani, President of Digital Media: We've talked about this in the context of p times q plus v in the past. You know, where p is new users bringing in more people into the franchise. […] the composition of growth is going to be a little different next year compared to FY2024. Again, the growth algorithm is new users, new products, and value and pricing. New users and new products will be a more significant part of the mix as we go into FY2025.

p. 7 · Read in context →

Guidance philosophy on AI: 'consumption' feeds ARR mainly through pricing tiers, not a metered model customers have to watch.

Keith Bachman (BMO); Shantanu Narayen, CEO: is that gonna be a contributor towards ARR growth, or should investors really be thinking about trying to match my seats, if you will, and really shouldn't it be about consumption being additive growth in 2025. […] you're gonna see, quote-unquote, consumption, add to ARR, in two or maybe three ways more so in 2025 than in 2024. […] So the intention is that consumption is what's driving the increased ARR, but it may be as a result of tier in the pricing rather than a consumption model where people actually have to monitor it.

p. 11 · Read in context →

Q1 FY2024 Earnings Call — March 14, 2024

The first call after the Figma deal collapsed — the $1B breakup fee lands this quarter — and the Q&A is dominated by the existential question of the era: does generative AI expand Adobe's market or hollow out its tools and seats? · Open the full transcript →

The bill for the failed $20B bet: a $1B Figma termination payment that cut GAAP EPS by $2.19 and a matching hit to operating cash flow.

Dan Durn, CFO: GAAP EPS came in lower due to the $1 billion payment resulting from the termination of the Figma transaction. Absent the termination payment, our cash flows from operations would have been $1 billion more, and GAAP EPS would have been $2.19 higher.

p. 4 · Read in context →

AI monetization, three ways: generative packs in Creative Cloud, a monthly Acrobat AI Assistant add-on, metered custom models in enterprise.

Shantanu Narayen, CEO: we have the generative packs, as you know, in Creative Cloud. I think you will see us more and more have that as part of the normal pricing and look at pricing because that's the way in which we want to continue to see people use it. I think in Acrobat, as you've seen, we are not actually using the generative packs. We're going to be using more of an AI Assistant model, which is a monthly model. As it relates to the Enterprise, we have both the ability to do custom models, which depends on how much content that they are creating, as well as an API and metering that we've rolled out and we've started to sell that as part of our GenStudio solution.

p. 8 · Read in context →

The core bull-vs-bear pivot: does AI raise or shrink Adobe's seat count? Narayen argues more models mean more interfaces, not fewer.

Keith Weiss (Morgan Stanley); Shantanu Narayen, CEO: The primary concern I hear from many is whether the emergence of AI and the growing number of models, whether for image or video, will lead to an increase or decrease in the number of seats for Adobe and beyond. I firmly believe that as we discuss these models and interfaces for creative content, the number of these interfaces will definitely rise. Therefore, Adobe must seize this significant opportunity. Overall, larger models will create even more opportunities for interfaces, and I think we are particularly well-suited to capitalize on that.

p. 14 · Read in context →

Q3 FY2022 Earnings Call — September 15, 2022

The landmark that set the terms of debate for years: the day Adobe announced its ~$20B bid for Figma. Management lays out the 'creativity on the web' rationale while analysts hammer the price, the dilution, and whether the organic engine still works. · Open the full transcript →

The announcement and the asset: a ~$400M-ARR, >150%-net-retention web design platform, bought to accelerate creativity on the web.

Shantanu Narayen, Chairman & CEO; David Wadhwani, President of Digital Media: I'm thrilled to share that today we announced our intention to acquire Figma, a leading web-first design platform that will help us accelerate this vision. […] Figma is expected to add approximately $200 million in net new ARR this year, surpassing $400 million in total ARR exiting 2022 with greater than 150% net-dollar retention rate. With the total addressable market of $16.5 billion by 2025, Figma is just getting started.

p. 3 · Read in context →

The terms that spooked the market: ~$20B, half cash/half stock, dilutive to non-GAAP EPS for two years, accretive only exiting year three.

Dan Durn, CFO: we've agreed to acquire Figma for approximately $20 billion comprised of approximately half cash and half stock, subject to customary adjustments. […] In year 1 and 2 after closing the transaction will be dilutive to Adobe's non-GAAP EPS, and we expect it to be breakeven in year 3 and accretive at the end of year 3.

p. 6 · Read in context →

The hardest question: is a $20B deal reactive, and is Adobe's organic engine still alive? Narayen: seize the decade-defining bet.

Brad Zelnick (Deutsche Bank); Shantanu Narayen, Chairman & CEO: what do you say to the perspective that this $20 billion acquisition seems more reactive versus proactive? And perhaps more importantly, how do we get comfortable that Adobe's organic-innovation engine is alive and well for capturing the trends and opportunities that lie ahead in Creative? […] I understand that in these markets, in particular, acquisitions and maybe large ones are viewed with some skepticism We certainly believe, and I'll talk about it, that Figma will be a transformative deal for the customers and industries. And it dramatically increases our TAM. We can deliver great value to an increasing set of customers. But I also want to reassure all of you, and if you look at our results, this in no way changes our focus or our excitement on our current portfolio.

We're growing well, and we're demonstrating strength across all of our 3 cloud offerings, and we continue to execute against our current initiatives And so if you look at the multiple internal businesses that are achieving velocity, whether it's Adobe Experience Platform and the apps that are built natively on top of it, what's happening with 3D and Immersive, what's happening with Acrobat Forms, what's happening with Frame.io. This is additive.

And when opportunities like this present themselves, Brad, I think it's the great companies that look at it and say, are you going to focus on the here and now only? Or are you going to seize on the opportunity that really positions Adobe for the next few decades?

p. 9 · Read in context →

More calls

Q1 FY2026 Earnings Call — March 12, 2026 · 13 pages · The last call before the freemium reset: the FY26 opening quarter under the new customer-group reporting, CC Pro migration and agentic-interface framing — a baseline for what changed one quarter later. · Open →

Q3 FY2025 Earnings Call — September 11, 2025 · 13 pages · Mid-year evidence that the AI story was ramping: accelerating AI-influenced/AI-first ARR and enterprise GenStudio/AEP momentum heading into the Firefly and Foundry launches at MAX. · Open →

Q2 FY2025 Earnings Call — June 12, 2025 · 14 pages · The quarter Adobe began breaking out an AI-first 'book of business' target and defended the pace of AI monetization against a de-rated stock. · Open →

Q1 FY2025 Earnings Call — March 12, 2025 · 14 pages · The first quarter reported under the new 'ending ARR book of business' methodology, with the standalone Firefly app and video generation moving from beta to market. · Open →

Q3 FY2024 Earnings Call — September 12, 2024 · 13 pages · A tight, two-analyst Q&A centered on AI Assistant adoption and Firefly Services — and the CEO's recurring 'AI expands our TAM' argument as the stock stayed under pressure. · Open →

Q2 FY2024 Earnings Call — June 13, 2024 · 14 pages · A beat that briefly rallied the stock: net-new Digital Media ARR reaccelerated and management pushed back on the AI-disruption narrative amid the Firefly terms-of-use controversy. · Open →

Q1 FY2023 Earnings Call — March 15, 2023 · 17 pages · The pre-Firefly baseline: strong Creative and Document Cloud results with the Figma deal still pending regulatory review, just before Adobe unveiled its generative-AI models. · Open →

Q2 FY2022 Earnings Call — June 16, 2022 · 18 pages · The quarter before the Figma bombshell — a clean read on Adobe's pre-acquisition, pre-GenAI growth model and how it framed macro and pricing at the time. · Open →

Adobe Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

Adobe Inc. — FY2025 Annual Report (Form 10-K) — FY2025 (year ended November 28, 2025)

Latest 10-K; recasts the whole business around AI and pre-announces the FY2026 collapse to a single reportable segment. · Open the full document →

Item 1. Business — p. 4 · Read the full section →

Management's own framing of the mission, the AI-era pivot, and a competitive field now including AI- and cloud-native entrants.

Mission and the AI-era strategy of commercially-safe first-party plus partner models.

Adobe’s mission is to empower everyone to create. We build innovative platforms and tools that unleash creativity, productivity and personalized customer experiences. […] In the artificial intelligence (“AI”) era, we are harnessing the power of AI across our solutions by bringing together our commercially safe first-party and leading partner AI models best suited for the job; deploying conversational and agentic capabilities across offerings; ensuring ubiquity on all surfaces; delivering trusted and secure solutions

p. 4 · Read in context →

How Adobe describes its competitive environment — including new AI or cloud-native entrants.

We participate in a highly competitive and rapidly evolving environment where our competitors include companies of various sizes and both public and private companies, including large, global companies and smaller companies with more specialized focuses, new entrants, and AI or cloud-native companies. […] The markets for our solutions are characterized by rapid technological innovation, new industry standards, evolving distribution and sales models, limited barriers to entry, short product lifecycles, customer price sensitivity, global economic conditions and the frequent entry of new solutions or competitors.

p. 8 · Read in context →

Item 1. Business — Segments — p. 18 · Read the full section →

The structural break: three segments in FY2025, consolidated into one reportable segment effective Q1 FY2026.

Three FY2025 segments — and the coming single-segment reorganization.

In fiscal 2025, our business consisted of three reportable segments: Digital Media, Digital Experience and Publishing and Advertising. […] Effective in the first quarter of fiscal 2026, we will combine our prior segments—Digital Media, Digital Experience and Publishing and Advertising—into a single operating and reportable segment due to changes in how management intends to evaluate results, allocate resources and execute the strategic opportunities outlined above.

p. 18 · Read in context →

Item 1A. Risk Factors — p. 28 · Read the full section →

The two risks specific to Adobe's moment: keeping pace with AI, and the liability of building and shipping AI itself.

Item 7. MD&A — Results of Operations — p. 56 · Read the full section →

Management explains fiscal 2025: subscription-led growth across both major offerings, with the revenue mix now ~96% subscription.

What drove fiscal 2025 — AI-powered differentiation feeding software-based subscription growth.

For our fiscal 2025, we experienced strong demand across our Digital Media and Digital Experience offerings, driven by transformative and customer-focused product innovation. As we execute on our long-term growth initiatives, with emphasis on delivering value through AI-powered and highly differentiated solutions to meet the needs of our diverse and expanding customer base, we have continued to experience growth in software-based subscription revenue across our portfolio of offerings.

p. 56 · Read in context →

Item 7. MD&A — Segment Information — p. 61 · Read the full section →

The segment revenue table and what management credits for the growth — Creative Cloud Pro, Acrobat, and GenStudio.

Named growth drivers for Digital Media subscription revenue.

The increase in subscription revenue for the Digital Media segment was driven by strength in Creative Cloud Pro and other flagship apps as well as Acrobat across all routes to market and geographies.

p. 61 · Read in context →

Note 1. Significant Accounting Policies — Revenue Recognition — p. 86 · Read the full section →

The accounting policy that defines the SaaS model: subscription and hosted revenue recognized ratably over the service term.

How Adobe recognizes hosted/subscription revenue — ratably over the contractual term.

Fully hosted subscription services (“SaaS”) allow customers to access hosted software during the contractual term without taking possession of the software. […] We recognize revenue ratably over the contractual service term, which typically ranges from 1 to 36 months, for hosted services that are priced based on a committed number of transactions where the delivery and consumption of the benefit of the services occur evenly over time, beginning on the date the services associated with the committed transactions are first made available to the customer and continuing through the end of the contractual service term.

p. 86 · Read in context →

More annual reports

Adobe Inc. — FY2024 Annual Report (Form 10-K) — FY2024 (year ended November 29, 2024) · 157 pages · Last full year on the classic three-segment reporting; Firefly ramping and the terminated Figma deal ($1.0B fee) behind it. · Open →

Adobe Inc. — FY2023 Annual Report (Form 10-K) — FY2023 (year ended December 1, 2023) · 157 pages · First 10-K to introduce Firefly generative AI, filed as the $20B Figma acquisition was being abandoned. · Open →

Adobe Inc. — FY2022 Annual Report (Form 10-K) — FY2022 (year ended December 2, 2022) · 164 pages · Announces the (later terminated) Figma acquisition agreement — a pre-generative-AI snapshot of the strategy. · Open →

Adobe Inc. — FY2021 Annual Report (Form 10-K) — FY2021 (year ended December 3, 2021) · 163 pages · Pre-Firefly, pre-Figma baseline of the Digital Media / Digital Experience subscription model. · Open →

Competitors describe Adobe Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

Figma (FIG)

The most direct competitor to Adobe's Creative Cloud design tools. Figma's collaborative interface- and product-design platform overlaps Adobe XD, Photoshop and Illustrator in UI/UX work and increasingly in creative-for-marketing — the overlap regulators judged so close that Adobe's ~$20 billion acquisition of Figma was abandoned in 2023. Figma's transcripts avoid naming Adobe; the by-name material sits in the merger disclosure.

Figma's own 10-K records the abandoned Adobe merger — Adobe agreed to acquire Figma in September 2022 and the two terminated in December 2023 citing no clear path to regulatory approval — the clearest evidence antitrust regulators viewed the two as head-on competitors.

On September 15, 2022, we entered into an Agreement and Plan of Merger (the "Merger Agreement") with Adobe, Inc. ("Adobe") and certain of Adobe’s wholly-owned subsidiaries. On December 17, 2023, we mutually agreed with Adobe to terminate the Merger Agreement based on the joint assessment that there was no clear path to obtain the required regulatory approvals for the transaction to close

p. 142 · Read in context →

CEO Dylan Field stakes out the 'design layer above code' — including creative design for marketing and advertising — as the 'battleground for how software gets built,' the same creative and experience territory Adobe occupies.

Dylan Field, Co-Founder and CEO: As code becomes more commoditized and easier to write, design is clearly the layer above code and visual thinkers outnumber those comfortable in a terminal or an IDE. We expect this space to continue to heat up and be the battleground for how software gets built. Tools around visual communication and creative design for marketing and advertising will be essential for breaking through the noise.

p. 7 · Read in context →

Figma quantifies adoption of its AI app-builder Figma Make — 70% quarter-over-quarter growth in weekly active users, use by over half of its >$100k-ARR customers, and nearly 60% of 2025 Make files created by non-designers (developers, PMs, marketers) — showing Figma reaching beyond designers into content creation.

Dylan Field, Co-Founder and CEO: Weekly active users of Figma Make grew over 70% quarter-over-quarter. And, as of Q4, over 50% of paid customers spending more than $100,000 in ARR were building in Figma Make on a weekly basis. […] of all Figma Make files created in 2025, nearly 60% were created by non-designers. We’re talking developers, PMs, marketers, and others inside the company

p. 2 · Read in context →

Docusign (DOCU)

The direct competitor to Adobe's Document Cloud e-signature product, Acrobat Sign. Docusign's FY2026 10-K names Adobe as its 'primary global competitor for eSignature' — the tab's premise realised in the peer's own words — and it is expanding from pure e-signature into 'intelligent agreement management,' a broader document-workflow ambition that overlaps Adobe's Document Cloud.

Docusign's FY2026 10-K names Adobe (Acrobat Sign) as its primary global e-signature competitor, alongside broader software companies embedding basic e-signature and contract-lifecycle-management vendors.

Our primary global competitor for eSignature is currently Adobe, which offers an electronic signature solution known as Adobe Acrobat Sign. We also face competition from other global software companies that have or may elect to include basic electronic signature capability in their products and from various vendors that focus on specific industries, geographies, or product areas such as contract lifecycle management and advanced contract analytics.

p. 18 · Read in context →

Docusign sizes the agreement-management opportunity at a $2 trillion global market it has begun addressing for tens of thousands of customers — the document-workflow ambition, beyond pure e-signature, that overlaps Adobe's Document Cloud.

Allan Thygesen, Chief Executive Officer: Agreement management is a $2 trillion global market problem, and over the past 18 months, we’ve helped tens of thousands of customers begin to solve it.

p. 2 · Read in context →

Asked directly about the competitive landscape, CEO Allan Thygesen reports little change in the e-signature market — stable share, Docusign perhaps performing slightly better — a level-headed read on the mature category where Adobe is its named rival.

Allan Thygesen, Chief Executive Officer (responding to Patrick Walravens, Citizens JMP): In our legacy markets, I see very little change in the competitive dynamics. The market share and our competitors have been stable, and we may actually be performing slightly better. The CLM space remains quite competitive, with several players in a small category, but we are managing to hold our own despite the competition. As we redefine and enhance our company vision, we are setting the pace. However, as we broaden our ambitions, we are encountering not only existing competitors but also other potential challengers. Overall, we are becoming a thought leader in the agreement space. Right now, I believe our focus should be on execution rather than competition, especially in the more established e-sign category.

p. 13 · Read in context →

Salesforce (CRM)

The principal competitor to Adobe's Digital Experience segment. Salesforce's Marketing Cloud, Commerce Cloud and — most pointedly — its Data Cloud / Data 360 customer-data platform contest the same marketer buyer Adobe serves with Experience Cloud, Journey Optimizer and Real-Time CDP. Salesforce does not name Adobe; the overlap is drawn from its own product and data-platform disclosures.

Salesforce describes its Marketing offering as a 'complete marketing platform' for lifecycle personalization built on unified customer profiles — the segmentation, journeys and AI-driven personalization that collide with Adobe Campaign, Journey Optimizer and Experience Platform.

Our Marketing offering is a complete marketing platform designed to help customers personalize engagement across the customer lifecycle. […] With operational customer profiles, marketers and AI agents can easily take action on structured and unstructured data to build segments, calculate insights, analyze performance, and power AI recommendations, decisioning, and automations.

p. 8 · Read in context →

CEO Marc Benioff frames the customer-data business as Salesforce's most strategic, citing a ~$7 billion Data Cloud with 140% year-over-year customer growth and over half the Fortune 500 onboard — the CDP layer that directly contests Adobe's Real-Time CDP.

Marc Benioff, Chair and Chief Executive Officer: I think the data business is probably the most strategic and most important business for Salesforce going forward. And already, it’s a $7 billion business, and data cloud is having a great year. It had a 140% year over year growth in customers and 326% growth in rows accessed by zero copy integration. […] But over half of the Fortune 500 are already on Data Cloud, but it’s really just the very, very beginning.

p. 3 · Read in context →

Microsoft (MSFT)

A broad platform competitor colliding with Adobe on generative-AI content creation. Microsoft now ships its own first-party image-generation model (MAI Image Two) inside Bing and PowerPoint and Copilot 'agent mode' that produces finished creative deliverables — encroaching on Adobe Firefly and Creative Cloud. Only the content-creation lines are used here; Azure, gaming and LinkedIn are excluded. Notably, Adobe appears in these calls as a Microsoft customer and ISV partner, not a named rival.

Microsoft touts MAI Image Two as 'one of the top image generation models in the world,' already generating images in Bing and PowerPoint and sold to creative customers like Shutterstock and WPP — a first-party challenge to Adobe Firefly and Adobe Stock.

Satya Nadella, Chairman and Chief Executive Officer: We introduced MAI Transcribe One, a state-of-the-art speech-to-text model, and MAI Image Two, one of the top image generation models in the world. These models are already powering first-party scenarios like image generation in Bing and PowerPoint […] We also brought MAI models to commercial customers like Shutterstock and WPP for the first time through Foundry.

p. 2 · Read in context →

Nadella bundles Microsoft's first-party text/voice/image models with Copilot 'Agent Mode' that turns prompts into export-quality PowerPoint and Word — and names Adobe among the ISVs building agents on Copilot, casting Microsoft as the platform beneath Adobe.

Satya Nadella, Chairman and Chief Executive Officer: When it comes to our first-party models, we are excited by the performance of our new MAI models for text, voice and image generation, which debuted among the top in the industry leader boards. […] This quarter, we also introduced Agent Mode, which turns single prompts into export-quality Word documents, Excel spreadsheets, PowerPoint presentations and then iterates to deliver the final product much like agent mode in coding tools today. […] We are seeing a growing Copilot agent ecosystem with top ISVs like Adobe, Asana, Jira, LexisNexis, SAP, ServiceNow, Snowflake and Workday, all building their own agents that connect to Copilot.

p. 2 · Read in context →

Microsoft reports Copilot as its fastest-adopted Microsoft 365 suite and names Adobe among customers buying over 25,000 Copilot seats in the quarter — a reminder that Adobe is a Microsoft customer even as Microsoft builds competing creative-AI tools.

Satya Nadella, Chairman and Chief Executive Officer: Customers continue to adopt Copilot at a faster rate than any other new Microsoft 365 suite, with strong usage intensity as shown by our week-over-week retention. And we saw the largest quarter of seat additions since launch with a record number of customers returning to buy more seats. […] And Adobe, KPMG, Pfizer, and Wells Fargo all purchased over 25,000 seats this quarter.

p. 2 · Read in context →

Autodesk (ADSK)

A design-software peer whose overlap with Adobe is narrow but real, concentrated in Media & Entertainment — Maya, 3ds Max and Flame for film, VFX and games sit alongside Adobe's video and 3D/Substance tools — plus the shared subscription model and generative-AI content push. Autodesk's core AEC/CAD business does not overlap Adobe and is excluded. Autodesk names Adobe in its 10-K competitor list.

Autodesk's FY2026 10-K lists Adobe first among its primary global competitors and, in the same section, flags AI as a force that could reshape its markets — the explicit by-name acknowledgment of the rivalry.

Our primary global competitors include Adobe Systems Incorporated, Bentley Systems, Inc., Dassault Systèmes S.A. and its subsidiary Dassault Systèmes SolidWorks Corp., Intergraph Corporation, a wholly owned subsidiary of Hexagon AB, MSC Software Corporation, Nemetschek AG, Oracle Corporation, Procore Technologies, Inc., PTC Inc., 3D Systems Corporation, Siemens PLM, and Trimble Navigation Limited, among others. […] Disruptive technologies such as machine learning and other AI technologies may significantly alter the market for our products in unpredictable ways and reduce customer demand.

p. 17 · Read in context →

Autodesk describes its Media & Entertainment Collection as 'end-to-end creative tools for entertainment creation' — Maya and 3ds Max for film, VFX and games — the creative-media territory adjacent to Adobe's video and 3D offerings.

Maya software provides 3D modeling, animation, effects, rendering, and compositing solutions that enable film and video artists, game developers, and design visualization professionals to digitally create engaging, lifelike images, realistic animations and simulations, extraordinary visual effects, and full-length animated feature films. […] The M&E Collection provides end-to-end creative tools for entertainment creation. This collection enables animators, modelers, and visual effects artists to access the tools they need, including Maya and 3ds Max, to create compelling effects, 3D characters, and digital worlds.

p. 8 · Read in context →

Oracle (ORCL)

A marketing/customer-experience applications competitor to Adobe's Digital Experience segment, though a thin one: Oracle's story is dominated by database and OCI cloud infrastructure, and its named applications rival is Salesforce, not Adobe. Its CX applications — including a new website generator and campaign tooling — are the piece that overlaps Adobe Experience Cloud. Database, OCI and hardware are excluded.

Oracle says it has built three new CX applications — including a website generator and lead/campaign tooling ('email opens') — the content-management and marketing-automation surface Adobe Experience Cloud sells, though Oracle frames the rivalry against Salesforce rather than Adobe.

Mike Sicilia, Chief Executive Officer: Embracing AI with small engineering teams, we have just built three brand new CX applications: lead generation and qualification, sales orchestration and automated selling, and our new website generator. […] We have built these new CX products to help our customers sell, not simply to administer a forecast or generate email opens. These are three products that Salesforce does not have.

p. 2 · Read in context →

Oracle's FY2026 10-K lists Adobe among the companies its cloud and software offerings 'compete directly with' — a boilerplate, conglomerate-wide naming rather than a CX-specific one, but Adobe named in Oracle's own filing.

Our enterprise cloud, software and hardware offerings compete directly with certain offerings from some of the largest and most competitive companies in the world, including Adobe Systems Incorporated, Alphabet Inc., Amazon.com, Inc., Cisco Systems, Inc., Intel Corporation, International Business Machines Corporation, Microsoft Corporation, Salesforce, Inc. and SAP SE

p. 18 · Read in context →

More peer documents

Q2_FY2025 — 11 pages · Dylan Field on the 'vibe coding / vibe designing' AI-prototyping wave and how Figma Make's design-context interoperability differentiates it — color on the emerging AI-creative competitive front. · Open →

DOCU_annual_report_FY2025 — 158 pages · Prior-year 10-K also names Adobe Acrobat Sign as the primary e-signature competitor and adds the 'Intelligent Agreement Management is a new software category without incumbent competitors' positioning — a two-year read on the by-name rivalry. · Open →

CRM_annual_report_FY2026 — 144 pages · Latest-year restatement of the Marketing/Commerce definitions plus 'Agentforce for Marketing' — briefs, content and journeys on unified 360-degree profiles — the freshest language on the Experience-Cloud overlap. · Open →

Q3_FY2026 — 15 pages · Benioff quantifies Data 360 (renamed Data Cloud) at 32 trillion records ingested and frames a ~$10 billion data layer (Data 360 + MuleSoft + Informatica) — a bigger, later sizing of the CDP business contesting Adobe Real-Time CDP. · Open →

MSFT_annual_report_FY2025 — 137 pages · Productivity & Business Processes segment and M365 Consumer 'productivity and creativity' framing — the 10-K context for Microsoft's creative-AI push, though generic and naming Apple/Google/Slack/Zoom rather than Adobe as rivals. · Open →

Q1_FY2026 — 16 pages · CEO Andrew Anagnost on Flow Studio (formerly Wonder Studio) — a 'highly disruptive direct-to-special-effects' generative video/VFX tool — the clearest Autodesk collision with Adobe Firefly/video AI in creative media. · Open →

Q2_FY2026 — 10 pages · Fusion CX growth (+12%) inside a ~$6 billion cloud-applications run-rate and Oracle's 'only complete application suites' positioning — sizes the small CX slice that overlaps Adobe against ERP/HCM/SCM. · Open →

Q4_FY2026 — 14 pages · CEO on IAM's competitive advantages (1,100+ integrations, data moat) and the ARR mix ($3.3 billion ARR, IAM 11%) — the platform-differentiation and scale context behind the e-signature rivalry with Adobe. · Open →

Source: S&P Capital IQ consensus via Xpressfeed · Generated 2026-07-18.

Street snapshot

The USD price target averages $272 (median $250) but spans a wide $190 to $380 across 33 estimates.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst counts shown explicitly; recommendation respondents: 39.

| Street view | Reading | Analysts |

|---|---|---|

| Recommendation mix | Buy 9, Outperform 2, Hold 24, Underperform 1, Sell 3 | 39 |

| Consensus score | 2.67 | 39 |

| Target price | mean 272.5; high 380.0; low 190.0 | 33 |

Forward table

Currency: USD · Scale: money in millions, absolute (per share) · Analyst count is the estimate count for each period and metric.

| Period | Metric | Mean | YoY | Analysts | Low / high |

|---|---|---|---|---|---|

| FY0E | Revenue | 26,518 | 11.6% | 30 | 25,810 / 26,737 |

| FY0E | EBITDA | 12,668 | 7.3% | 8 | 12,330 / 12,904 |

| FY0E | EBIT | 11,951 | 9.2% | — | — / — |

| FY0E | Net income (GAAP) | 7,212 | 1.2% | 17 | 7,013 / 7,484 |

| FY0E | Net income (normalized) | 9,671 | 8.5% | — | — / — |

| FY0E | EPS (GAAP) | 18.10 | 8.4% | 16 | 17.55 / 18.78 |

| FY0E | EPS (normalized) | 24.42 | 16.6% | 31 | 24.25 / 24.99 |

| FY0E | Free cash flow | 10,371 | 11.3% | — | — / — |

| FY0E | Dividend per share | 0.00 | — | — | — / — |

| FY0E | Gross margin | 89.9% | -0.2% | — | — / — |

| FY0E | Capital expenditure | -218.1 | 1.3% | — | — / — |

| FY0E | Net debt | -768.9 | -40.1% | — | — / — |

| FY0E | ROE | 74.6% | 23.1% | — | — / — |

| FY0E | Cash from operations | 10,497 | 10.7% | — | — / — |

| FY+1E | Revenue | 28,891 | 8.9% | 30 | 28,350 / 29,812 |

| FY+1E | EBITDA | 13,651 | 7.8% | 8 | 13,090 / 14,252 |

| FY+1E | EBIT | 12,936 | 8.2% | — | — / — |

| FY+1E | Net income (GAAP) | 8,148 | 13.0% | 17 | 7,474 / 8,812 |

| FY+1E | Net income (normalized) | 10,456 | 8.1% | — | — / — |

| FY+1E | EPS (GAAP) | 21.35 | 18.0% | 16 | 19.99 / 23.61 |

| FY+1E | EPS (normalized) | 27.53 | 12.7% | 32 | 25.66 / 29.15 |

| FY+1E | Free cash flow | 11,240 | 8.4% | — | — / — |

| FY+1E | Dividend per share | 0.00 | — | — | — / — |

| FY+1E | Gross margin | 89.5% | -0.4% | — | — / — |

| FY+1E | Capital expenditure | -268.5 | 23.1% | — | — / — |

| FY+1E | Net debt | -4,662 | 506.4% | — | — / — |

| FY+1E | Cash from operations | 11,516 | 9.7% | — | — / — |

| FY+1E | ROE | 71.5% | -4.3% | — | — / — |

| FY+2E | Revenue | 31,384 | 8.6% | 15 | 30,587 / 33,344 |

| FY+2E | EBITDA | 14,575 | 6.8% | 5 | 13,934 / 14,997 |

| FY+2E | EBIT | 14,105 | 9.0% | — | — / — |

| FY+2E | Net income (GAAP) | 9,124 | 12.0% | 8 | 8,638 / 9,995 |

| FY+2E | Net income (normalized) | 11,366 | 8.7% | — | — / — |

| FY+2E | EPS (GAAP) | 24.72 | 15.8% | 8 | 22.97 / 28.50 |

| FY+2E | EPS (normalized) | 31.45 | 14.3% | 15 | 29.35 / 34.94 |

| FY+2E | Free cash flow | 12,168 | 8.3% | — | — / — |

| FY+2E | Dividend per share | 0.00 | — | — | — / — |

| FY+2E | Gross margin | 89.3% | -0.1% | — | — / — |

| FY+2E | Capital expenditure | -327.0 | 21.8% | — | — / — |

| FY+2E | Net debt | -3,277 | -29.7% | — | — / — |

| FY+2E | ROE | 67.4% | -5.7% | — | — / — |

| FY+2E | Cash from operations | 12,758 | 10.8% | — | — / — |

| Q3 FY2026 | Revenue | 6,695 | 11.8% | 27 | 6,597 / 6,764 |

| Q3 FY2026 | EBITDA | 3,140 | 5.3% | 8 | 3,005 / 3,248 |

| Q3 FY2026 | EBIT | 2,953 | 9.6% | — | — / — |

| Q3 FY2026 | Net income (GAAP) | 1,769 | -0.2% | 14 | 1,678 / 1,894 |

| Q3 FY2026 | Net income (normalized) | 2,403 | 9.0% | — | — / — |

| Q3 FY2026 | EPS (GAAP) | 4.48 | 7.2% | 14 | 4.25 / 4.80 |

| Q3 FY2026 | EPS (normalized) | 6.08 | 14.5% | 28 | 5.82 / 6.35 |

| Q3 FY2026 | Free cash flow | 2,184 | 4.9% | — | — / — |

| Q3 FY2026 | Dividend per share | 0.00 | — | — | — / — |

| Q3 FY2026 | Gross margin | 89.9% | -0.3% | — | — / — |

| Q3 FY2026 | Capital expenditure | -61.00 | -0.6% | — | — / — |

| Q3 FY2026 | ROE | 83.6% | 16.1% | — | — / — |

| Q3 FY2026 | Cash from operations | 2,184 | 3.9% | — | — / — |

| Q4 FY2026 | Revenue | 6,832 | 10.3% | 26 | 6,510 / 6,957 |

| Q4 FY2026 | EBITDA | 3,192 | 6.1% | 8 | 2,978 / 3,310 |

| Q4 FY2026 | EBIT | 3,024 | 8.7% | — | — / — |

| Q4 FY2026 | Net income (GAAP) | 1,849 | -0.4% | 14 | 1,734 / 1,988 |

| Q4 FY2026 | Net income (normalized) | 2,459 | 8.7% | — | — / — |

| Q4 FY2026 | EPS (GAAP) | 4.75 | 6.7% | 14 | 4.45 / 5.12 |

| Q4 FY2026 | EPS (normalized) | 6.32 | 14.9% | 28 | 5.88 / 6.62 |

| Q4 FY2026 | Free cash flow | 3,193 | 21.6% | — | — / — |

| Q4 FY2026 | Dividend per share | 0.00 | — | — | — / — |

| Q4 FY2026 | Gross margin | 89.7% | -0.4% | — | — / — |

| Q4 FY2026 | Capital expenditure | -55.56 | -11.7% | — | — / — |

| Q4 FY2026 | Cash from operations | 3,187 | 17.1% | — | — / — |

| Q4 FY2026 | ROE | 82.7% | 7.9% | — | — / — |

| Q1 FY2027 | Revenue | 6,988 | 9.2% | 22 | 6,896 / 7,163 |

| Q1 FY2027 | EBITDA | 3,395 | 5.8% | 6 | 3,159 / 3,554 |

| Q1 FY2027 | EBIT | 3,212 | 8.9% | — | — / — |

| Q1 FY2027 | Net income (GAAP) | 2,029 | 7.4% | 12 | 1,893 / 2,229 |

| Q1 FY2027 | Net income (normalized) | 2,617 | 8.3% | — | — / — |

| Q1 FY2027 | EPS (GAAP) | 5.21 | 13.4% | 12 | 4.89 / 5.82 |

| Q1 FY2027 | EPS (normalized) | 6.73 | 11.1% | 24 | 6.39 / 7.08 |

| Q1 FY2027 | Free cash flow | 2,938 | 27.9% | — | — / — |

| Q1 FY2027 | Dividend per share | 0.00 | — | — | — / — |

| Q1 FY2027 | Gross margin | 89.6% | -0.5% | — | — / — |

| Q1 FY2027 | Capital expenditure | -59.11 | 11.4% | — | — / — |

| Q1 FY2027 | Cash from operations | 3,061 | 28.4% | — | — / — |

| Q1 FY2027 | ROE | 91.4% | 11.2% | — | — / — |

| Q2 FY2027 | Revenue | 7,203 | 8.8% | 22 | 7,095 / 7,448 |

| Q2 FY2027 | EBITDA | 3,355 | 6.9% | 6 | 3,085 / 3,512 |

| Q2 FY2027 | EBIT | 3,198 | 11.4% | — | — / — |

| Q2 FY2027 | Net income (GAAP) | 2,020 | 18.0% | 12 | 1,892 / 2,121 |

| Q2 FY2027 | Net income (normalized) | 2,604 | 11.2% | — | — / — |

| Q2 FY2027 | EPS (GAAP) | 5.23 | 23.1% | 12 | 4.91 / 5.63 |

| Q2 FY2027 | EPS (normalized) | 6.80 | 14.1% | 24 | 6.49 / 7.11 |

| Q2 FY2027 | Free cash flow | 2,432 | 7.0% | — | — / — |

| Q2 FY2027 | Dividend per share | 0.00 | — | — | — / — |

| Q2 FY2027 | Gross margin | 89.4% | -0.5% | — | — / — |

| Q2 FY2027 | Capital expenditure | -64.64 | 16.5% | — | — / — |

| Q2 FY2027 | ROE | 86.0% | 2.1% | — | — / — |

| Q2 FY2027 | Cash from operations | 2,550 | 18.7% | — | — / — |

Estimate momentum

The upgrades have largely stalled in the last 30 days, where both revenue and EPS marks are essentially flat.

Currency: USD · Scale: money in millions, absolute (per share) · Point-in-time consensus; analyst count is shown where supplied.

| Period | Metric | Lookback | Then | Now | Direction / magnitude | Analysts |

|---|---|---|---|---|---|---|

| 2028 | Revenue | 30d | 31,437 | 31,384 | down 0.2% | — |

| 2028 | Revenue | 90d | 31,097 | 31,384 | up 0.9% | — |

| 2028 | Revenue | 180d | 30,628 | 31,384 | up 2.5% | — |

| 2027 | EPS (normalized) | 30d | 27.54 | 27.53 | down 0.0% | — |

| 2027 | EPS (normalized) | 90d | 26.31 | 27.53 | up 4.6% | — |

| 2027 | EPS (normalized) | 180d | 26.34 | 27.53 | up 4.5% | — |

| 2028 | EPS (normalized) | 30d | 31.54 | 31.45 | down 0.3% | — |

| 2028 | EPS (normalized) | 90d | 29.29 | 31.45 | up 7.4% | — |

| 2028 | EPS (normalized) | 180d | 28.78 | 31.45 | up 9.3% | — |

| 2027 | Revenue | 30d | 28,901 | 28,891 | down 0.0% | — |

| 2027 | Revenue | 90d | 28,421 | 28,891 | up 1.7% | — |

| 2027 | Revenue | 180d | 28,365 | 28,891 | up 1.9% | — |

Beat / miss record

Adobe has topped consensus on both revenue and normalized EPS in each of the last eight quarters. The EPS surprises have run the larger of the two, roughly +1.7% to +3.2%, while revenue beats have been narrower at about +0.6% to +2.6%.

Current sequences by metric: Revenue: 8 consecutive beats; EPS (normalized): 8 consecutive beats.

Currency: USD · Scale: money in millions, absolute (per share) · Consensus is captured before each actual first became effective; analyst count shown per observation.

| Quarter | Metric | Consensus as of | Actual | Surprise | Outcome | Analysts |

|---|---|---|---|---|---|---|

| Q2 FY2026 | Revenue | 6,451 | 6,618 | 2.6% | Beat | — |

| Q2 FY2026 | EPS (normalized) | 5.81 | 5.96 | 2.5% | Beat | — |

| Q1 FY2026 | Revenue | 6,277 | 6,398 | 1.9% | Beat | — |

| Q1 FY2026 | EPS (normalized) | 5.87 | 6.06 | 3.2% | Beat | — |

| Q4 FY2025 | Revenue | 6,111 | 6,194 | 1.4% | Beat | — |

| Q4 FY2025 | EPS (normalized) | 5.40 | 5.50 | 1.9% | Beat | — |

| Q3 FY2025 | Revenue | 5,909 | 5,988 | 1.3% | Beat | — |

| Q3 FY2025 | EPS (normalized) | 5.18 | 5.31 | 2.5% | Beat | — |

| Q2 FY2025 | Revenue | 5,805 | 5,873 | 1.2% | Beat | — |

| Q2 FY2025 | EPS (normalized) | 4.97 | 5.06 | 1.7% | Beat | — |

| Q1 FY2025 | Revenue | 5,662 | 5,714 | 0.9% | Beat | — |

| Q1 FY2025 | EPS (normalized) | 4.97 | 5.08 | 2.2% | Beat | — |

| Q4 FY2024 | Revenue | 5,541 | 5,606 | 1.2% | Beat | — |

| Q4 FY2024 | EPS (normalized) | 4.67 | 4.81 | 3.0% | Beat | — |

| Q3 FY2024 | Revenue | 5,373 | 5,408 | 0.6% | Beat | — |

| Q3 FY2024 | EPS (normalized) | 4.54 | 4.65 | 2.5% | Beat | — |

Where the street disagrees

Out-year earnings estimates widen as coverage thins — FY2028 normalized EPS spans $29.35 to $34.94 across 15 contributors and FY2029 rests on just one to two estimates — while EBITDA is covered by only a handful of analysts throughout.

Currency: USD · Scale: money in millions, absolute (per share) · Dispersion is high-low divided by absolute mean; analyst count shown per item.

| Period | Metric | Mean | Low | High | Spread / mean | Analysts |

|---|---|---|---|---|---|---|

| 2028 | EPS (GAAP) | 24.72 | 22.97 | 28.50 | 22.4% | 8 |

| Q1 FY2027 | EPS (GAAP) | 5.21 | 4.89 | 5.82 | 17.9% | 12 |

| 2028 | EPS (normalized) | 31.45 | 29.35 | 34.94 | 17.8% | 15 |

| 2027 | EPS (GAAP) | 21.35 | 19.99 | 23.61 | 17.0% | 16 |

| Q1 FY2027 | Net income (GAAP) | 2,029 | 1,893 | 2,229 | 16.6% | 12 |

Source: Visible Alpha consensus via S&P Xpressfeed · Consensus as of 2026-07-14 · generated 2026-07-18.

Model trust

FY-2025 is the last actual year, with FY-2026 through FY-2028 estimated.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Coverage depth and vintage; broker count is the maximum represented.

| Brokers | Line items | Last revision |

|---|---|---|

| 24 | 403 | 2026-07-14 |

Operating KPIs

Coverage on these lines is thinner than the P&L, at roughly 5 to 17 brokers versus 20-plus on revenue, so the ARR path reads as indicative rather than firm.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · FY-1A / FY0E / FY+1E; broker count shown per KPI.

| Operating KPI | Source | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|---|

| Net cash provided by/(used for) investing activities | CD | -1,009,722.12bn Amount | -1,293,337.68bn Amount | -349,359.02bn Amount | 24 |

| Revenue | CD | 23,687,876.96bn Amount | 26,528,381.78bn Amount | 28,856,659.00bn Amount | 24 |

| Cash and cash equivalents at beginning of period | CD | 7,753,150.60bn Amount | 5,303,803.00bn Amount | 6,689,992.59bn Amount | 23 |

| Depreciation, amortization and accretion | CD | 801,010.09bn Amount | 763,302.23bn Amount | 791,349.74bn Amount | 23 |

| Net cash provided by/(used for) financing activities | CD | -10,055,915.33bn Amount | -7,532,670.42bn Amount | -7,932,879.96bn Amount | 23 |

| Net cash provided by/(used in) operating activities | CD | 9,497,310.22bn Amount | 10,622,862.03bn Amount | 11,633,324.71bn Amount | 23 |

| Purchases of property and equipment | CD | 261,614.71bn Amount | 237,194.62bn Amount | 280,852.61bn Amount | 23 |

| Cash and cash equivalents | CD | 5,605,524.63bn Amount | 7,054,628.28bn Amount | 11,564,463.98bn Amount | 22 |

| Debt | CD | 5,869,340.91bn Amount | 4,955,388.89bn Amount | 4,955,388.89bn Amount | 22 |

| Effect of foreign currency exchange rates on cash and cash equivalents | CD | 39611681.8% | 3165450.0% | 2012000.0% | 22 |

| Free cash flow | CD | 9,221,848.49bn Amount | 10,394,946.58bn Amount | 11,321,514.29bn Amount | 22 |

| Free cash flow/share($) | CD | 21.51 Amount | 26.02 Amount | 29.60 Amount | 22 |

P&L bridge

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Margins are derived against revenue; YoY compares adjacent fiscal columns; broker count shown per line.

| P&L line | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|

| Revenue | 23,687,876.96bn Amount | 26,528,381.78bn Amount (12.0% YoY) | 28,856,659.00bn Amount (8.8% YoY) | 24 |

| Gross Profit | 21,364,625.20bn Amount (90.2% margin) | 23,876,583.11bn Amount (90.0% margin; 11.8% YoY) | 25,875,978.38bn Amount (89.7% margin; 8.4% YoY) | 23 |

| Ebitda | 11,629,235.82bn Amount (49.1% margin) | 12,697,563.31bn Amount (47.9% margin; 9.2% YoY) | 13,742,242.51bn Amount (47.6% margin; 8.2% YoY) | 22 |

| Operating Income | 10,838,984.23bn Amount (45.8% margin) | 11,938,835.18bn Amount (45.0% margin; 10.1% YoY) | 12,946,103.95bn Amount (44.9% margin; 8.4% YoY) | 23 |

| Net Income | 8,838,925.96bn Amount (37.3% margin) | 9,734,217.31bn Amount (36.7% margin; 10.1% YoY) | 10,538,467.13bn Amount (36.5% margin; 8.3% YoY) | 22 |

| Eps | 20.60 Amount | 24.37 Amount (18.3% YoY) | 27.52 Amount (12.9% YoY) | 22 |

Consensus dispersion

The pattern points to margin and capital-return conversion, not revenue, as the open question.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Top high-low spreads relative to absolute mean; requires at least 3 brokers.

| Line item | Period | Mean | Min | Q1 | Q3 | Max | Spread / mean | Brokers |

|---|---|---|---|---|---|---|---|---|

| Net cash provided by/(used for) investing activities | 4QFY-2025 | -51,265.84bn Amount | -238,250.00bn Amount | -75,000.00bn Amount | -60,950.00bn Amount | 531,449.83bn Amount | 1501.4% | 21 |

| Net cash provided by/(used for) investing activities | 4QFY-2026 | -80,729.42bn Amount | -491,219.18bn Amount | -68,254.79bn Amount | -50,375.82bn Amount | -15,737.86bn Amount | 589.0% | 18 |

| Effect of foreign currency exchange rates on cash and cash equivalents | FY-2026 | 3165450.0% | -12691000.0% | 4000000.0% | 4000000.0% | 4000000.0% | 527.3% | 20 |

| Net cash provided by/(used for) investing activities | FY-2028 | -523,452.91bn Amount | -2,879,527.00bn Amount | -345,770.87bn Amount | -232,185.55bn Amount | -137,571.58bn Amount | 523.8% | 13 |

| Net cash provided by/(used for) investing activities | FY-2027 | -349,359.02bn Amount | -1,720,233.00bn Amount | -327,088.84bn Amount | -225,021.40bn Amount | -112,568.67bn Amount | 460.2% | 20 |

| Net cash provided by/(used for) investing activities | 3QFY-2025 | -77,210.35bn Amount | -275,500.00bn Amount | -69,971.55bn Amount | -48,239.93bn Amount | -44,437.50bn Amount | 299.3% | 19 |

Quarterly path

These forward ARR lines rest on only 5 to 7 brokers, so the quarterly KPI path is less firmly held than revenue and EPS.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Next four supplied quarters; final column is maximum broker coverage in the row.

| Quarter | Net cash provided by/(used for) investing activities | Revenue | Cash and cash equivalents at beginning of period | Depreciation, amortization and accretion | Net cash provided by/(used for) financing activities | Total revenue | EPS Diluted, Applicable to common stockholders($) | Broker coverage |

|---|---|---|---|---|---|---|---|---|

| 3QFY-2026 | -66,092.14bn Amount | 6,691,254.58bn Amount | 4,918,751.56bn Amount | 213,045.29bn Amount | -2,004,422.22bn Amount | 6,691,254.58bn Amount | 6.07 Amount | 20 |

| 4QFY-2026 | -80,729.42bn Amount | 6,818,360.30bn Amount | 5,392,311.53bn Amount | 211,150.53bn Amount | -2,011,874.54bn Amount | 6,818,360.30bn Amount | 6.28 Amount | 20 |

| 1QFY-2027 | -60,963.70bn Amount | 6,974,491.61bn Amount | 6,703,167.09bn Amount | 204,531.11bn Amount | -2,160,319.09bn Amount | 6,974,491.61bn Amount | 6.73 Amount | 20 |

| 2QFY-2027 | -66,071.80bn Amount | 7,191,656.44bn Amount | 7,908,579.19bn Amount | 205,898.11bn Amount | -2,000,718.42bn Amount | 7,191,656.44bn Amount | 6.78 Amount | 20 |

23 stale period values omitted; 0 line items fully removed.

Source: S&P Capital IQ transcripts via Xpressfeed · latest indexed call 2026-06-11 · generated 2026-07-18.

Latest call digest

Adobe Inc., Q2 2026 Earnings Call, Jun 11, 2026 · 2026-06-11T21:00:00

Q2 FY2026 — June 11, 2026. Adobe posted record revenue of $6.62B (+11% YoY constant currency) and non-GAAP EPS of $5.96, and raised full-year revenue and non-GAAP EPS targets (now including the Semrush acquisition, ~$480M of ARR). But the prepared remarks and the Q&A told two different stories. Management's message was strategic: with adobe.com traffic up 35–50% YoY and AI reshaping how users discover products, Adobe is pivoting hard to a freemium/MAU-first acquisition model — expanding free Firefly, Express and Acrobat onboarding, and deferring previously planned Creative Cloud line (price) optimizations. AI-first ARR crossed $500M (3x YoY) and Firefly ARR grew ~50% QoQ toward ~$300M. The cost: the total-Adobe ARR growth target was framed at 10.2% and management explicitly conceded the pivot lowers second-half ARR from individual subscribers. Overlaying this, CFO Dan Durn is departing (Steve Day named interim CFO) while the CEO search continues as Shantanu Narayen moves toward Board Chair. The Q&A was pointed and repetitive: analysts pressed on why now, the payback on the roughly half-billion-dollar ARR give-up, the durability of free-user LTV, and — from the other direction — whether Adobe should be pivoting even harder. Management leaned on early Firefly/Express traction and the Reader-era freemium playbook, but offered directional rather than precise payback math ("play out over 2027").

Participant coverage from the latest call.

| Group | Participants | Count |

|---|---|---|

| Management | Operator; Douglas Clark — Vice President of Investor Relations, Adobe Inc.; Shantanu Narayen — Chairman & CEO, Adobe Inc.; David Wadhwani — President of Creativity & Productivity Business, Adobe Inc.; Anil Chakravarthy — President of Customer Experience Orchestration Business, Adobe Inc.; Steven Day — Interim CFO and Senior VP of Finance, Technology, Security & Operations, Adobe Inc. | 6 |

| Analysts | Michael Turrin — Equity Analyst, Wells Fargo Securities, LLC, Research Division; Aleksandr Zukin — MD & Head of the Software Group, Wolfe Research, LLC; Matthew Swanson — Analyst, RBC Capital Markets, Research Division; Brad Zelnick — MD of Software Equity Research & Senior US Software Research Analyst, Deutsche Bank AG, Research Division; William Fitzsimmons — Senior Research Analyst, Piper Sandler & Co., Research Division; S. Kirk Materne — Senior MD & Fundamental Research Analyst, Evercore ISI Institutional Equities, Research Division; Brent Thill — MD & Tech Sector Equity Analyst, Jefferies LLC, Research Division; Saket Kalia — Senior Analyst, Barclays Bank PLC, Research Division | 8 |

Curated latest-call exchanges; one row per analyst topic.

| Analyst | Firm | Topic | What changed in Q&A |

|---|---|---|---|

| Michael Turrin | Wells Fargo Securities | CEO & CFO transition | Opened on managing continuity with both a CEO search and a CFO departure in motion, and the profile needed for the next chapter. Narayen stressed a seasoned finance bench and said Adobe 'won't miss a beat.' |

| Aleksandr Zukin | Wolfe Research | Freemium timing & ARR payback | Hardest exchange: challenged why freemium flipped from a second-half tailwind to a headwind, and asked the payback period/multiple on the ~$0.5B organic ARR give-up. Management pointed to early MAU/Firefly signals but framed payback qualitatively as playing out over 2027 rather than a specific figure. |

| S. Kirk Materne | Evercore ISI | Free-user LTV & stickiness | Asked how they get comfortable on long-term economics of free users. Wadhwani cited higher engagement and conversion for search-led free users versus direct-to-paid, but conceded it 'needs time to play out.' |

| Brent Thill | Jefferies | Pace of the pivot | Pushed from the opposite side — why not pivot harder and build a bigger moat, invoking the subscription transition. Narayen said Adobe is spending on models, marketing and product and 'will not be short-term focused,' but keeping discipline. |

| Brad Zelnick | Deutsche Bank | Co-opetition with AI platforms | On partnering versus competing with Google/OpenAI/Anthropic building their own design tools. Management framed cloud-spend partnerships and argued rivals are focused on code while Adobe is the 'company of one' on consumer creativity. |

| Matthew Swanson | RBC Capital Markets | Semrush / brand visibility | How Semrush fits the portfolio. Chakravarthy described marrying Semrush's outside-in query data with Adobe's content (AEM) for generative-engine-optimization brand visibility, to be unveiled at Cannes Lions. |

| William Fitzsimmons | Piper Sandler | Moats, M&A & buyback | On AI-era moats (20 years of data, governance/auditability) and appetite for tuck-in M&A alongside the new $25B authorization. Narayen said it is a good time for technology tuck-ins as many AI companies lack sustainable models. |

Theme tracker

Themes are curator-classified across supplied calls.

| Theme | Status | Quarters mentioned | Read-through |

|---|---|---|---|

| Firefly & generative-AI monetization | persisted | Q3 2023, Q4 2023, Q1 2024, Q2 2024, Q3 2024, Q4 2024, Q1 2025, Q2 2025, Q3 2025, Q4 2025, Q1 2026, Q2 2026 | Present on every call in the window. The framing evolved from image-generation volume and generative credits (2023–24) to a standalone Firefly app, credit packs and enterprise Firefly Services, with Firefly ARR approaching $300M by Q2 2026. |

| AI-first / AI-influenced ARR disclosure | emerged | Q1 2025, Q2 2025, Q3 2025, Q4 2025, Q1 2026, Q2 2026 | New disclosure begun in Q1 2025 (>$125M AI-first book of business), then repeatedly quantified — $250M target achieved early in Q3 2025, AI-influenced ARR past $5B, AI-first ARR >$500M by Q2 2026. Became the primary lens for the AI narrative. |

| Freemium / MAU-first acquisition pivot | emerged | Q4 2025, Q1 2026, Q2 2026 | Freemium existed for Acrobat/Express earlier, but the strategic pivot that explicitly accepts a near-term ARR trade-off to maximize MAU is new to late FY2025–FY2026 and dominates the Q2 2026 call. Freemium/MAU references rose sharply across the last three calls. |

| Creative Cloud pricing & line optimizations | persisted | Q4 2023, Q1 2024, Q2 2025, Q3 2025, Q1 2026, Q2 2026 | A recurring ARR lever — renewal price uplift and tiering (Creative Cloud Pro). In Q2 2026 management reversed course and deferred previously planned second-half line optimizations, calling it a phase shift rather than a cancellation. |

| Enterprise CXO / GenStudio / agentic marketing | persisted | Q3 2023, Q4 2023, Q1 2024, Q2 2024, Q4 2024, Q1 2025, Q2 2025, Q3 2025, Q4 2025, Q1 2026, Q2 2026 | The Digital Experience / enterprise story recurs every call, migrating from AEP and native apps to GenStudio content supply chain and, by FY2026, agentic Customer Experience Orchestration plus the Semrush deal. |

| Macro / consumer & advertising demand | dropped | Q3 2023, Q4 2023, Q2 2024, Q1 2025 | Macro jitters, consumer spend and (in Q1 2025) tariffs were a recurring analyst and management topic through early FY2025, then faded to near-absence by FY2026 as the conversation shifted entirely to AI and freemium. |

| Leadership transition (CEO & CFO) | emerged | Q1 2026, Q2 2026 | Absent from the earlier record, then emerged in Q1 2026 (Narayen's move toward Board Chair and CEO search) and intensified in Q2 2026 with CFO Dan Durn's departure and Steve Day's interim appointment. |

Guidance ledger

Quotes, calls, and speakers are source-verified; outcomes are curator-classified.

| Verbatim guidance | Call | Speaker | Curator outcome | Outcome note |

|---|---|---|---|---|

| “And we expect this AI book of business to double by the end of fiscal '25.” | Adobe Inc., Q1 2025 Earnings Call, Mar 12, 2025 · 2025-03-12T21:00:00 | Shantanu Narayen | kept | The AI-first book of business was >$125M exiting Q1 2025; by Q3 2025 management said the new AI-first products had already achieved the end-of-year target of over $250M. |

| “Digital Media net new ARR of approximately $550 million” | Adobe Inc., Q3 2024 Earnings Call, Sep 12, 2024 · 2024-09-12T21:00:00 | Daniel Durn | kept | The Q4 2024 target was met — Adobe reported net new Digital Media ARR of $578M for Q4 FY2024. |

| “For FY '25, we're targeting total Adobe revenue of $23.30 billion to $23.55 billion” | Adobe Inc., Q4 2024 Earnings Call, Dec 11, 2024 · 2024-12-11T22:00:00 | Daniel Durn | kept | The FY25 range was raised across the year and exceeded; Adobe reported record FY2025 revenue of $23.77B. |

| “This is the foundation for our FY '26 Total Adobe ARR growth target of over 10%” | Adobe Inc., Q4 2025 Earnings Call, Dec 10, 2025 · 2025-12-10T22:00:00 | Shantanu Narayen | pending | FY2026 is in progress; by Q2 2026 the total-Adobe ARR growth target was set at 10.2%, reflecting Semrush plus the freemium pivot and deferred line optimizations. |

| “For FY '26, we are targeting total Adobe revenue of $26.5 billion to $26.6 billion.” | Adobe Inc., Q2 2026 Earnings Call, Jun 11, 2026 · 2026-06-11T21:00:00 | Steven Day | pending | Raised full-year target set on the latest call (includes Semrush); FY2026 not yet complete in the supplied history. |

Q&A pressure map

Question counts and firms are curator tallies; analyst coverage shown above.

| Topic | Questions | Firms | Pressure / response |

|---|---|---|---|

| Freemium pivot & near-term ARR trade-off | 6 | Wells Fargo Securities, Wolfe Research, Evercore ISI, Jefferies, Barclays | The dominant line of questioning on the Q2 2026 call — why accelerate freemium now, the payback on the ~$0.5B ARR give-up, free-user LTV/stickiness, and whether to pivot even harder. On the direct payback-period question, management gave directional color (playing out over 2027) rather than the specific payback/multiple asked for. |

| Guidance conservatism & net-new-ARR modeling | 5 | Jefferies, Deutsche Bank, Wolfe Research, UBS, Morgan Stanley | On the Q1 2024 call, after a smaller-than-usual beat, multiple analysts pressed why the full-year guide wasn't raised and how to model the impact of price increases inside reported ARR; management reaffirmed rather than lifted the outlook. |

| When AI meaningfully moves revenue | 4 | Jefferies, Wolfe Research, JPMorgan | Recurring through FY2025, anchored by the Q1 2025 opener asking when the AI book of business becomes more than a low-single-digit percent of revenue; management answered with the new AI-first ARR disclosures and the doubling target. |

| Creative Cloud pricing / line optimization impact | 3 | Citigroup, Evercore ISI, Wells Fargo Securities | Analysts repeatedly probed the reaction to Creative Cloud Pro pricing and line-item optimizations (Q2 2025, Q3 2025), culminating in the Q2 2026 question on why deferring the increase is the right call. |

Language shifts

Only language evidence verified against the referenced component is shown.

| Observation | Verbatim evidence | Call ID | Component |

|---|---|---|---|

| New, explicit acknowledgment that the strategy sacrifices near-term ARR — a marked change from the prior beat-and-raise register that had emphasized record net new ARR. | “This shift will come at the cost of short-term ARR, but will accelerate user acquisition in MAU” | 1996469811 | 3 |

| Guidance language turned from raising and reaffirming targets to openly guiding a component of ARR lower — a meaningful shift in confidence framing on subscriber ARR. | “lowers our second half ARR growth expectations from individual subscribers” | 1996469811 | 2 |

| For contrast, as recently as Q4 2025 the CFO framed FY2026 in unqualified confident terms, underscoring how the Q2 2026 trade-off language is a genuine change in tone. | “we are confident in our ability to deliver industry-leading innovation, double-digit ARR growth and world class profitability” | 1967943306 | 5 |

The call history reframes the current debate: Adobe's execution and guidance track record has been strong (AI-first and net-new-ARR targets were repeatedly met or exceeded), but Q2 2026 marks a deliberate break — trading near-term subscriber ARR for freemium-driven MAU, deferring price optimizations, and doing so amid a CEO search and CFO change. The investment question shifts from 'can they hit the number' to 'will the freemium bet convert to durable monetization before the ARR give-up is felt.'

The Cash Franchise

Adobe sells the software that professionals use to make and manage digital content, almost entirely by subscription. Over a decade revenue quadrupled to $23.8 billion, roughly 96% of it recurring, and the business converted about 40 cents of every revenue dollar into free cash flow — $9.9 billion in fiscal 2025. Yet the stock has fallen about two-thirds from its 2021 peak even as that cash flow rose. This chapter establishes what the company is, how it earns, and why the gap exists.

What Adobe sells